Comments

Results from UChicago EA's Personal Finance Workshop

17 min readMar 19, 2022

Acknowledgements (in surname alphabetical order): Many thanks to Isaac Dunn and Aaron Gertler for providing feedback on this post.

Also, this was written in November and so any thoughts on future directions for UChicago EA may no longer be relevant, as I will not be organizing after May.

On Nov 12, 2021, UChicago EA ran our first-ever personal finance workshop. This was an introductory workshop, assuming almost zero prior knowledge (except about the existence of the stock market, stocks, etc.). We primarily covered investing, with brief mentions of budgeting and selecting the right bank and tax-advantaged accounts. This was deliberate given that the core audience was UChicago undergraduates, who most likely do not have tax-advantaged accounts but can make immediate changes to their budgeting, personal banking, and investing behavior.

The workshop consisted of a casual ~45 minute presentation with audience questions throughout. You can access our slides here and an audio recording, including an auto-generated transcript, here (starting from slide 7).

There were nine attendees, six of whom are currently participating in our Introductory Fellowship. Every attendee filled out the feedback form. The form was, by default, anonymous although attendees could choose to leave their email to be contacted.

Note: I attended an EA retreat in January that has shifted some of my views on university community building (specifically, more towards disproportionately spending effort on a select group of students and very deliberately creating programming optimized for their needs). I am fairly—though not completely—confident that the following rationale holds despite my recent update.

Universally recommendable: Personal finance provides a way for everyone, regardless of career or socioeconomic status, to optimize the altruistic potential of their dollars. This improves the accessibility of the EA approach to finance: you don’t have to take a lucrative job to maximize the impact of your money. Aside from income, the other primary way to gain wealth is investment, and leaving it untapped runs counter to optimizing the altruistic potential of one’s wealth.

Trialling a different kind of structured engagement → Provide valuable information; possibly find a more effective way of increasing retention: As a university community-builder, I aim to find the best ways to create a campus community that aspiring EAs want to continually engage with. I think these ‘non-EA-but-framed-in-an-EA-way’ skill workshops help fill a desire from students who lack a sense of agency re: making an impact (e.g., because they have yet to start working) while demonstrating what living according to EA principles might look like.

Drawing from my own experiences with close-knit campus communities, I suspect that discussing ‘life skills’ is a common way of increasing support within and connection to a group. Yet, these kinds of events don’t seem very common amongst EA university groups (or at least, not that I’ve heard of). I am also drawing from interesting friend groups I know, which hold regular presentations/discussion on topics and essentially function as a casual, fun learning community. I think that kind of environment might be conducive for EA university groups and that regular skills workshops could be more successful than the previously-tried model of weekly knowledge-sharing presentations (usually on a cause area).[1]

Broadly, I feel somewhat confident (60%) that this more holistic programming is a cost-effective way to increase the connection that students feel with their university groups. This workshop represents one way in which I tried to test that hunch.

Note: I am not confident that workshops are the optimal form of ‘life skills’ programming, as opposed to general low-effort, high-return life advice.

Framing your EA group as one that cares about members besides their impact: Running life-skills workshops that are not solely centered around members’ direct impact suggests that the group is interested in holistically supporting its members, rather than only being focused on their ability to do good.

It is possible that this may not be a good thing - perhaps EA would be more effective if it were only associated with social impact and its members encouraged to seek out support with other aspects elsewhere. I have stated two cases (weak and strong) for framing EA more holistically below.

The weak version is focused on a specific group: perhaps providing more holistic programming helps give your university group an edge. For example, if your group emphasizes social events as a crucial means of retention and other social groups provide this kind of holistic programming, then you may also want to incorporate such programming. Note that this could also go the other way - perhaps your group only wants to be seen as a resource for directly discussing how best to do good.

The strong version is focused on EA: perhaps EA, overall, could increase its impact if it provided more holistic support. This belief underlies, for example, the EA Infrastructure Fund’s grants to Ewelina Tur and Sebastian Schmidt. Quoting Michael Aird, who evaluated those two grants:

“... both grants are intended to improve the grantees’ ability to help promising, EA-aligned people to have more impact over their careers.” So, providing holistic programming could indirectly improve members’ effectiveness.

A related but subtler point relates to perceptions of EA. If members care about joining groups that appear to care about them outside of direct EA engagement, to the extent that the presence of more holistic programming significantly affects recruitment or retention, then providing such programming may be a net benefit regardless of its instrumental value to members’ impact.

Regardless, I think the meta-EA case does not hinge on whether you believe EA should be more or less holistic.

Increasing donation potential: Our rationale stems from the ability for smarter investing to indirectly have a multiplier effect on one’s donation ability, by directly having a multiplier effect on one’s wealth. However, the impact of this workshop is not equal to the difference in wealth—rather, this workshop’s impact stems from getting people to change from saving to investing and (more realistically) shifting up the age at which someone would begin investing [smartly].

For example, one participant had been investing an average of $1500 a year. We estimated that, if they applied the investing principles from our workshop, we would have ~doubled (2.18x) their holdings. (Assumptions below)

Increasing long-term sustainability: Financial security is also a key part of general life satisfaction and potentially for sustaining altruistic efforts (e.g., maintaining a level of self-care).

All data was collected via a feedback form that participants filled out at the end of the workshop, and hence is self-reported.

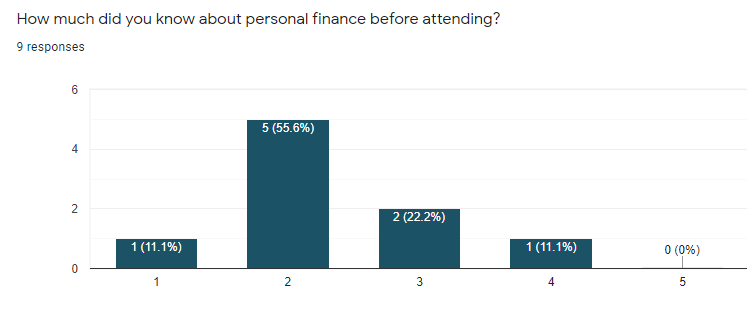

Knowledge of personal finance increased by ~1.

Note: I had too much fun making this form and used silly labels for these two questions (on personal finance knowledge).[2] So, this isn’t really useful data but I am including it as a directional indicator.

Knowledge of personal finance increased from a mean of 2.3 to 3.7. There was also less variation in these answers: initially, there was a range of 3 which dropped to 2.

All participants were likely to implement the skills they learned.

This question labeled 1 as “Definitely will not” and 5 as “Definitely will.”

Most (77.8%) respondents indicated that this workshop changed their financial plans, particularly for investing.

Given the workshop’s focus on investing, it seems promising that most of these responses were about investing.

We also asked a few optional questions.

One respondent expressed interest in a day-trading workshop. We are not confident this would be a net positive and have no plans to hold this, though I wonder if this suggests that our participants may be skewed towards a higher risk profile.

Epistemic status: Extremely low; this section is primarily speculative.

It is plausible that most of the impact of this workshop stems from its meta-EA impact. This is likelier if you assume that community building at target universities is, right now, a highly impactful thing to do. This assumption may be motivated by the community’s funding overhang and recent investments in community building. These suggest that

Thus, the direct impact of this personal finance workshop may be relatively less important than the meta-EA impact of helping create more HEAs (by increasing members’ engagement).

Unfortunately, I don’t have a great sense for the meta-EA impact of this workshop.

Drawing from our qualitative responses, it seemed that the participants enjoyed the workshop: everyone said that the workshop satisfied their expectations and 87.5% (7) respondents reported increased interest in these types of events. Furthermore, in the freeform comments and outside of this specific survey, several participants have mentioned that this was one of their favorite events of ours.[3] However, we did not ask about more relevant metrics of engagement, such as their feelings of belonging to the community or perception of UChicago EA.

As far as I can tell, the workshop didn’t affect the participants’ engagement with UChicago EA (e.g., event attendance), so it seems like this workshop was probably no better or worse than our regular socials for predicting or increasing EA engagement. The Introductory Fellowship is clearly a superior option, though that was a very strong prior for me (i.e., I never intended for this workshop to replace a fellowship). Furthermore, I don’t think comparing workshops to either socials or fellowships is the most appropriate: I believe that workshops should be additional to those two types of programming and should not take priority over them. Thus, the more appropriate comparison might be workshops to [a one-day conference / whatever EA Cambridge calls them] or a reading group. This is a difficult comparison for us to draw since we have yet to run much programming besides fellowships or socials, though our previous efforts at book clubs and weekly discussions/presentations generated very low engagement, so I am tentatively optimistic that workshops may be more effective for UChicago EA than weekly book or presentation discussions.[4]

Even if these workshops do not appear better than our socials, I am still keen to continue trialling them to test whether they truly are a worse/better option for creating HEAs. I am confident that the value of this workshop primarily manifests as an experiment with community-building strategy, and am curious to see which kinds of workshops may be better for increasing engagement. Intuitively, I think the type of workshop that would be most likely to increase engagement may be, say, a self-care workshop that generates more prosocial feelings than this finance-oriented workshop.

Since the impact from this workshop stems primarily from getting people to invest, and not getting them to invest better, I have focused only on the participants that had not previously been investing.

I took two approaches for estimating the potential impact of this workshop, both based on counterfactuals. Firstly, I estimated the difference in donation ability under two scenarios: optimistic (where a participant switches to investing solely because of this workshop) and pessimistic (where a participant invests earlier because of this workshop). Secondly, I used data provided by respondents about their actual donating/investing habits to try and estimate our impact more granularly.

I had two optional questions about how much participants were already donating/investing a year. Responding to one did not mean you had to respond to another. I received four valid (i.e., non-zero) responses each for donating and for investing, but one respondent skipped the donation question. Thus, I assumed that they were not donating regularly and gave them an annual donation of $0 in our calculations.

The rare best-case: The difference in return between holding $20,000 in a savings account (1% rate of return) and investing it (10% rate of return) is, over 40 years, $875,407.84.[6] Considering EA’s current funding situation, this might not be impressive. For an individual who is not earning-to-give, however, this may significantly augment their personal impact potential. However, this scenario represents the rare best-case for our workshop’s impact: this scenario assumes that our participants would never have implemented a similar investing strategy in the future, and so our workshop is fully responsible for causing this increase in their wealth. We do not anticipate this to be the case for the majority of our participants.

The more realistic case: For somebody who would have invested using a similar strategy, only later in time, the exact impact depends on the counterfactual delay. According to a 2014 Gallup poll, roughly half of Americans started investing in their twenties. Assuming that we sped it up ~3 years (i.e., participants would have used similar investing practices when exiting college, around the age of 22), then we would only have increased their holdings by 34%. This is approximately equal to increasing the rate of return by 1 percentage point, from 10 to 11%.

There is only one respondent who said that they had not already been investing. Assuming that after this workshop they choose to invest the equivalent of their annual donations, then in 40 years…

Respondent 5[7]

Donating prior: $1000, Investing prior: $0

→ Holdings without our workshop: $0

→ Holdings with our workshop: $45,259.26[8]

This is infinitely greater than their original investment, of course, but that’s not really useful. More importantly, this respondent already has a history of donating and so may be likelier to use their new wealth for altruistic purposes.

Two other respondents indicated that they were not already investing or donating, which is why they were not included here. In the best-case scenario (i.e., they invest according to our recommendations), they would strengthen our expected impact because the largest counterfactual impact stems from participants who were not investing pre-workshop and started investing post-workshop. Naively, we could estimate the impact of getting these two respondents to start investing as being similar to the impact of the rare best-case. Conservatively, I am assuming that the three non-respondents were already investing but suboptimally.

Finally, the benefit I am most confident in is the potential to increase the wealth of our members. However, this relates to both meta-EA and direct impact: increased wealth can increase the financial security of our members, which in turn can improve their wellbeing and sustain their engagement in EA (assuming that engagement in EA would generally be compromised if one needed to give higher weight to fiscal considerations). Increased wealth can also increase the donation potential of our members, increasing the direct impact of their charity. So, the benefit I am most confident in can bolster both the meta-EA and direct cases for running this workshop.

If your group has access to an appropriate speaker, then running a Personal Finance workshop could be a low-effort way of multiplying your members’ donation potential. Generally, investing is a universally recommendable thing—in the US, for example, most people have 401(k)s, which are joint retirement and investment plans—but since investment strategies may have wildly varying payoffs, it can be impactful to spend ~1 hour outlining the most reliable strategy (i.e., investing in the total stock market).

More broadly, I’m encouraged by this feedback to host more workshops oriented around practical life skills, and hope that other university community-builders will consider trialling this kind of programming. Even outside of the survey, attendants have reiterated that this workshop was one of the events they most enjoyed. This seems to align with my anecdotal experience: for example, underclassmen are eager to learn about navigating university life and will often ask upperclassmen for advice around workload, classes, etc. Thus, I hope to host future workshops on life skills that may be particularly relevant to EAs. Right now, I’m thinking of hosting a workshop on productivity or self-care.[9]

I would love to hear suggestions on how these trials could be improved, or general feedback on whether this kind of programming seems valuable for community building!

Orthogonally, I’d be curious to see if regular lightning talks might also be an effective type of social programming.

“Couldn't budget to save a dime!” as ‘1’ and “In line to be the next billionaire” as ‘5’

At that time, UChicago EA’s other programming consisted of the Introductory Fellowship and weekly unstructured socials.

We are branching out for the rest of the year, though, so I may have more thoughts a few months later!

This rate is extremely variable, so in the interest of being conservative, I have chosen a high rate that reflects some of the better savings account rates you could find.

The return from a 1% rate over 40 years is $9777.27, while the return from a 10% rate is $885,185.11

The other respondents had previously been investing.

Calculated using https://www.calculator.net/investment-calculator.html

For efficiency reasons, these might take place during a post-fellowship retreat that UChicago EA is co-planning with Northwestern, UW-Madison, and UMichigan. I would be interested, however, to see whether these life skills/holistic events are better fits for certain contexts (e.g., retreats or more ‘social’ environments).

The outline has some unexpected items (e.g., "Regardless [...]"). I checked in the editor and they are set to 'Paragraph,' so I'm not sure what's happening there!