My firing from the hip guess is that the lifetime effects of having more money to donate effectively dwarfs the extra harm caused by a bank investing slightly more money in bad things. The intuition mostly comes from the idea that a) the harmful investments aren't trying to cause the most harm, but your donations are (or should be) aimed at doing the most good, and b) I'd guess that if there is an evil thing with a good return, it'll be invested in anyway, whether your bank can do it or not (whereas a great charity with a good impact return generally has a major funding gap).

Keen to hear any updates I should make to my from-the-hip model here. I currently don't worry too much about what my bank does with my money, as long as I get a decent return.

Presumably customer deposits are typically invested in short term government paper and reverse repos rather than corporates. I would expect this to be similar across all banks.

(Also I disagree with classifying defence companies as immoral. This is the sort of thinking that leads the west to be vulnerable to aggressive dictatorships).

You can look at banks' financial reports. Santander's (https://www.santander.co.uk/assets/s3fs-public/documents/Santander%20UK%20plc%202024%20Annual%20Report.pdf) says £60 billion in "Cash, repos, other financial assets and other assets non-interest earning" and £176 billion in customer deposits.

This is a Draft Amnesty Week draft. It may not be polished, up to usual standards, fully thought through, or fully fact-checked.

I'm posting this to get it out there. I'd love to see comments that take the ideas forward. I wouldn't have posted without the nudge of Draft Amnesty Week. Fire away! (But be nice, as usual) I’m not using an Epistemic Status for this post - just think that this isn’t my field of expertise, though I did subscribe to the magazine Ethical Consumer for several years, but still might be wrong about this. Written for a UK perspective but can’t imagine other countries are immune to the incentives banks in the UK have.

Hey EA Forum reader, what bank account do you use? Why do you use them? Is it because you signed up for them over a decade ago and haven’t thought about it since[1]? There’s a good chance that’s why.

Going back to earlier days of EA, it would look at cause areas as how neglected they were, how tractable they were and how important the area is.

It’s my view that moving banks hits the neglected and tractable goals, and skims perilously close to a threshold of importance. And when it’s so straightforward, it feels like an easy and worthwhile thing to do.

The problem with banks

Banks, as you probably know, are the powerhouses of the economy, and lend money to people and businesses to fund projects and the like. Banks have a range of places they can invest their money, and some of these opportunities are worse for the world than others.

What kind of worse?

Banks typically and logically will invest your money into whatever is most profitable. A lot of the time that can be fossil fuels, weapons (including autonomous drones), deforestation causing industries, animal exploitation and tobacco.

As an example of how much funding goes into these sectors, the campaign Feedback found “Between 2015 and 2020, global meat and dairy companies received over $478 billion in backing by over 2,500 investment firms, banks, and pension funds headquartered around the globe.”

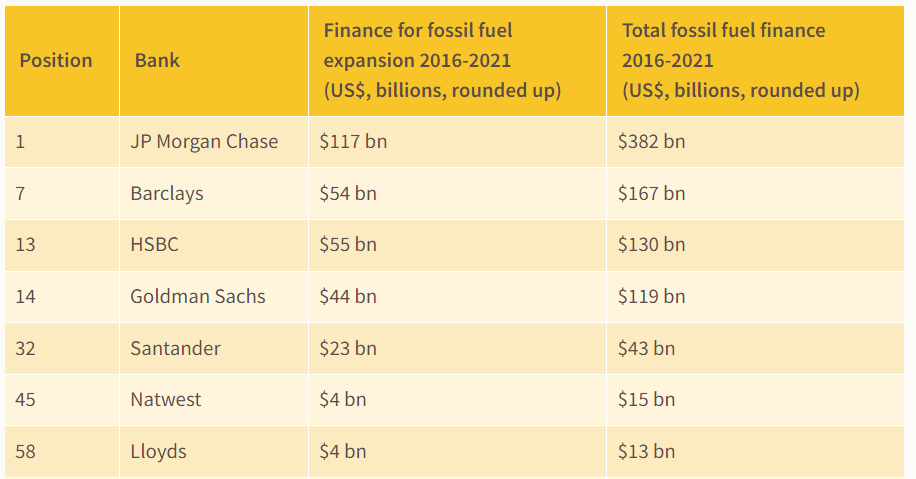

And the Banking on Climate Chaos report shows the scale of fossil fuel funding[2];

But you can be sure that unless a bank has a policy against funding some of these, they will be doing it - even places like Natwest have “restricted” sectors that they continue to fund, with the only restriction being some additional audits. Some of these projects are “fully-autonomous armed unmanned aerial vehicles” and “non-harmful child labour” - what a phrase.

The effect of switching banks

First and foremost you can be more confident that your money is not directly going to the net negative sectors discussed previously. The most positive evidence I could find for this is from moving your pension, which isn’t a million miles away from moving your bank account. Make My Money Matter state that changing your pension to green funds could decrease your carbon footprint by more than 21 times the combined effect of going vegetarian[3], stopping flying and changing energy providers, which frankly seems too good to be true (and my LLM of choice thinks that it is also too good to be true - it does suggest that’s a ceiling if the best case scenario of moving your pension works). For other measures of how your positive impact would change from switching banks, I failed to find much concrete data, this would be addressed in a follow up if I write it.

There’s also the chance of causing a sea change in the banking industry - A student boycott of Barclays in 1986 led to them to pull out of apartheid era South Africa [4]

How do I change my bank then?

Fortunately, in the UK, the current account switching service is available at the link. Your friend and mine Martin Lewis has a page on the best deals that are currently available for switching your current account - at time of writing (October 2025) there’s just Nationwide and Coop that offers a switching bonus, and are listed as one of the top 3 ethical banks by Ethical Consumer (see below).

It’s worth pointing out as well that if you have a current account that you like using, you don’t have to move that - just consider where your savings or stocks are kept. Wherever the bulk of your money is has the biggest effect through the bank.

Reviews of the switching service have generally been positive with people saying how easy it is. Consider that if you’re one of these people who stay with a bank for 17 years, even an hour of faff switching bank, would lead to 17 years of more positive impact with your money.

Trade-offs

Here’s what I have noticed after trying to use ethical banks for a while;

Generally lower interest rate/returns on stocks. I would estimate between 1-2% lower through an ethical bank than the alternative.

Apps and products are less competitive - Triodos, one of the most ethical options doesn’t even have a credit card, and neither Triodos or Co-op give you payment notifications such as Monzo does

Fewer physical branches (though this is happening across the sector)

My response to these

Yep, there’s no way around lower interest rates. However, I’ve also heard from a friend in finance that savings accounts are a way to lose money slower, as an amount of interest is wiped out by inflation anyway. With regards to stocks not gaining value as quickly as alternatives, you might consider it as a form of donating/tithing, that you will gain less money, but in the mean time your money (that is still your money, after all!) is doing much more good than it would do in whatever account/stocks that would give the biggest return

Since I’ve started paying for things through Google Wallet, I get payment by payment notifications which helps with one of these. Whilst I would like to use the most ethical bank for all my financial products, I don’t see an issue with using the next most ethical bank for e.g. a credit card. Regardless, don’t let perfect be the enemy of good

This might just be me, but I haven’t needed to go into a branch for a while - last cheque I got I actually posted to my bank with my details on a post-it note and it got paid in with no issues

Which banks are actually ethical?

This list is produced by the magazine Ethical Consumer, which rates on a positive and negative rating out of 20. I have some issue with their rating (until recently, they marked “support nuclear power” as a straight negative) but I think it is a good ballpark.

Triodos - Most transparent ethical policy, publishes all investments, focuses on renewable energy and organic farming. No branches and no switching bonus but highest ethical standards.

Nationwide - Building society (member-owned, not shareholder-driven). Clear ethical stance against weapons and fossil fuels. Offers branches and decent app experience.

Co-operative Bank - Strong ethical policy since 1992, avoids fossil fuels, arms trade. Recently strengthened their ethical stance.

Monzo are surprisingly high up on this ranking - I’ve been told by a FinTech guy that because it’s relatively new it’s being buoyed by investment funding and it doesn’t have to invest in certain places to report profit to shareholders, so it’s liable to change.

Next on my to do list is changing your energy supplier

“A student boycott of the bank led to a drop in its share of the UK student market from 27 per cent to 15 per cent by the time it pulled out.” a percentage change which I find inspiring and probably frankly well outside of what system change we could cause at the present moment, but it gives a flavour of the scope of change that can be achieved with fairly easy steps. https://www.independent.co.uk/news/business/news/barclays-faces-apartheid-court-action-340003.html

I used AI to fix transcription errors, rerrarange the ideas, and suggest tweaks to the title and some sentences.

Three of the most exciting projects to come out of EA in recent years are, in a vague sense, CEA spinouts:

* Kairos is directly a spinout of CEA and now handles most support for university AI safety groups. Basically everyone I've found who knows them is really excited about what they do

* NEST is an opinionated ideas-fi...

This post presents the executive summary from Giving What We Can’s impact evaluation for 2025. At the end of this post we share links to more information, including the full report and...

My firing from the hip guess is that the lifetime effects of having more money to donate effectively dwarfs the extra harm caused by a bank investing slightly more money in bad things. The intuition mostly comes from the idea that a) the harmful investments aren't trying to cause the most harm, but your donations are (or should be) aimed at doing the most good, and b) I'd guess that if there is an evil thing with a good return, it'll be invested in anyway, whether your bank can do it or not (whereas a great charity with a good impact return generally has a major funding gap).

Keen to hear any updates I should make to my from-the-hip model here. I currently don't worry too much about what my bank does with my money, as long as I get a decent return.