Comments

Great article, thanks! I wonder if the work by Follow This fits the definition: https://www.follow-this.org/

Great article, thanks! I wonder if the work by Follow This fits the definition: https://www.follow-this.org/

Thank you!

Yes, they get people to buy shares through their platform and then do shareholder activism based on all the shares their members have. Would be an interesting model to consider for animal advocacy groups focused on shareholder activism.

I'm looking for a diversified investment fund that engages in shareholder activism in a systematic way. Basically a Vanguard MSCI World, but with hundreds of lawyers whose only job is to push corporate agendas for the common good. In your research, did you come across any firms or products that I could take a look at? I've been doing a quick search once a year for some time now, but so far, I haven't found anything attractive that works for me as a retail investor.

Unfortunately, I'm not aware of something like that.

The first shareholder case in the USA was the suit filed by Peter Lovenheim of the Humane Society of the U.S. against Iroquois Brands in 1985. The company argued that Foie Gras was too small a part of their business to be the focus of a shareholder lawsuit but the SEC disagreed and held that the shareholder action could proceed.

Andrew Rowan, WellBeing International

Oh, that's an interesting case that I hadn't heard of! Nice, it seems to have been successful as well. Thanks for your comment, Andrew.

For others who are curious, this paper discusses the case: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1467949

TL;DR: Shareholder activism has shown a great deal of promise in general with inherent strengths, such as an automatic mechanism for being heard and for getting demands met. This contrasts with other methods of advocacy where these must be earned. It has already seen some victories within animal advocacy and has seen very substantial victories in other areas.

You can also read this report on Animal Ask's website.

Many thanks to Scott Behmer for reviewing this report and for the experts who generously lent their time during the interview process.

Shareholder activism[1] is a method of achieving change by buying the shares of corporations and leveraging the rights associated with that partial ownership. It has seen increasing use over the years, including many cases where the principal motivation is the public good, rather than corporate reform to maximise shareholder profit.

Shareholder activism relies on the unappreciated fact that, fundamentally, corporations are owned by their shareholders and there are automatic rights associated with that. It can be seen as the ultimate form of insider activism, since the approach reliably gives you the opportunity to talk directly with company board members.

Depending on the number of shares owned, there are a number of formal mechanisms to achieve this change. Shareholder activism is possible with remarkably few shares in the company as independent shareholders may be enlisted to support the proposal. However, this requires awareness and buy-in from the other shareholders, and so shareholder activism benefits from coordination with a broader campaign on the subject to provide that.

Shareholder activism should be done as part of an expert and dedicated group, or at least in coordination with one, since there are specific procedures that must be followed to avoid having the proposal dismissed on a technicality, and thereby block future advocacy attempts on that issue.

Shareholder activism has seen tremendous success as an advocacy tool with some significant successes relating to animal advocacy. The literature on shareholder activism generally supports this picture.

Furthermore, we think there are opportunities to increase the amount of shareholder activism work being done for animal advocacy, though this should be done carefully as there are risks associated with any cavalier implementation of shareholder activism, including from lack of coordination with existing shareholder activist groups.

Shareholder activism has contributed to notable successes, though the precise causality is often not certain. The Shareholder Action Guide (Behar 2016) describes some of these cases:

The successes have accumulated over a relatively short period of time. Shareholder activism has not been used much historically, but may have become much more common and effective in recent years. For example, Ertimur et al. (2010) found that the fraction of proposals receiving majority support increased from 10% in 1997 to more than 30% in 2003 to 2004. This could be due to large scandals and corporate governance in 2001 and 2002 (such as Enron) which propelled corporate governments into a central concern with obvious material implications on shareholder value.

Since then, the use of shareholder activism has continued to grow with the global financial crisis of 2008 perhaps inspiring more widespread use of the tactic (Interest 2015). In the US, there were 511 recorded events of shareholder activism recorded by Activist Insight in 2022, compared to 462 in 2021 (Insightia and Wolosky 2023).

Based on this evidence, Ferri (2015) concludes that low-cost shareholder activism (shareholder activism that does not depend on a large equity stake in the companies in question) is now a powerful tool.

The main requirements for running a shareholder activism campaign are[2]:

The stock ownership requirement is remarkably low, and successful shareholder activism has indeed been achieved with this low level of ownership; however, note that success rates increase when the shareholder activist owns a larger share of the company (Kölbel et al. 2019).

Once these conditions are met, you may file a shareholder resolution which is a request to the company for a reform or for further research for a proposed reform (to be presented to other shareholders).

There are strict rules of the form that shareholder resolutions must take. For example, there is a strict character limit of 500 characters in the statement of the resolution and it must not contain any false or misleading statements. If criteria such as these are not met, the resolution can be thrown out on a technicality (Behar 2016). For this reason it is important that it be done by a professional team with knowledge of the intricacies of shareholder activism (Behar 2016).

Other than the staff time, the cost of shareholder resolutions can be very low, though that cost can climb dramatically if advocacy methods are used alongside it, such as targeted ads (expert interviews).

Once the resolution is formulated and submitted, it is voted on by the shareholders who have a number of votes according to their proportional ownership of the company. Resolutions must achieve at least 5% support in the first year in order to be retabled at the next year’s shareholder meeting or 15% in the second, and 25% in subsequent years (USSIF, n.d.). For particularly important reforms, it could be damaging if this threshold is not met and other groups are not able to raise this issue again.

Shareholder resolutions typically receive less than 10% approval (Sjöström 2008). Indeed, in a typical year, only 10% to 20% of shareholder proposals that were put to a vote received over 20% approval by the shareholders (Hallaj 2013). However (and fortunately), resolutions do not need to achieve majority support to prompt company action, since it may be easier for the company to acquiesce rather than risk even partial alienation of its shareholders and the reputational risk they are concerned with. Indeed, even 10% approval for a shareholder resolution indicates significant dissent within the company, equivalent to a very large shareholder of the company disagreeing with company policy (“Shareholder Advocacy as a Tool for Change” 2020; Behar 2016).

Plausibly, some initial impact can come just by raising the issue with the company and shareholders who might not be familiar with these concerns. This can be true especially in emerging markets where concerns around animal agriculture are less well-known. Many of the groups we spoke with reported at least being able to raise the issue and have meetings with board members concerning the proposed reforms (expert interviews).

If the company does not back down, and the shareholder activist organisation decides it wants to push its case, the situation can escalate into a proxy fight. In a proxy fight, the shareholder activist team attempts to get other shareholders on side and vote out some or all of the board of directors, replacing them with others who are sympathetic to the animal welfare reforms in question and who will work to implement them. This represents a very significant escalation compared to simply resubmitting a shareholder resolution.

As described, proxy fights are extremely expensive, costing an average of $1.8 million (with a high of 25 million) for the shareholder and $3.9 million (with a high of $35 million) for the company (Levin 2022). These costs come from attorneys, bankers, public relations, consultants, among other advisors, as well as from proxy solicitation. A bare-bones campaign might be able to be run for $10,000 by electronically delivering proxy materials and not paying for most of these services, but this would be unlikely to succeed (Ellis 2023).

Because of these costs, it is uncommon for shareholder activism campaigns to come down to a proxy fight. In the data set that Naaraayanan et al. (2020) analysed, only one third of shareholder engagements went to a vote. It is more common for one of the sides to acquiesce. In some ideal cases, such as cases where the reform is not costly or where it brings substantial benefits, the shareholder action may be agreed to without too much pressure.

At least in harder cases, shareholder activism can be viewed as a game of chicken where the activists and those they are trying to convince both try to resolve the issue in their favour without having to pay the costs of a proxy conflict.

Significant legal help is required to engage in shareholder activism. This is in order to formulate the shareholder actions in the specific required manner, bring lawsuits against recalcitrant companies and manage legal liability in the actions of the shareholder activist organisation itself (Odene and Ozden, n.d.; Chen, n.d.).

In cases where directly asking for the change may be too ambitious, a shareholder campaign can start more modestly and less directly by asking for a report to be written discussing the risks of the harmful policy in question. This is easier to achieve and can still get things moving in the right direction (Behar 2016).

Another common shareholder activism tactic is to ask for the appointment of new board members in the company who are friendly to the desired reforms (Weinstein, de Wied, and Richter 2019). The new board members can help make other desired changes, and generally move the company forward in the desired direction. This can also be helpful in creating a more lasting change in the company decision-making, which can have ongoing benefits.

Altogether, the basic requirements are quite easy to state, but there are some very important intricacies that must be kept in mind when doing shareholder activism. This, combined with the risks of getting important reforms thrown out means that it is very important that shareholder activism be done in a careful and deliberate way with coordination with other shareholder activism groups (Behar 2016).

Shareholder activist campaigns are valuable in diversifying the lines of pressure and advocacy. If a company is only being pressured by external groups, it may not be as convincing as if they were also hearing it from people involved with their company. Hearing it from many distinct and diverse sources gives the sense that it is part of a much larger societal trend in that direction.

In this way, shareholder activism campaigns may work best when they are run alongside other animal advocacy campaigns also pushing for the reform in question. A broader campaign can make shareholders aware of the issue and cause them to form some opinion on it.

A broader campaign creates a sense that social change on the issue is imminent, and so the company might as well get off to an early start on it, rather than being ignominiously forced into that position at a later point. Ultimately, in most cases when shareholder animal activism is successful, it will be because shareholder activism successfully convinces the company that the public is on their side, which will be much easier when the reform in question is generally in the spotlight (Hallaj 2013).

It may also be particularly valuable in allowing specific asks to be introduced and negotiated on. Groups operating on the outside may be able to apply general pressure for reform, but if these efforts are to be successful, groups must at some point sit down and work out the details, while groups working on the outside in a more combative way are less likely to get this opportunity.

As such, there should be collaboration, communication, and coordination between shareholder activists and those running a broader campaign. This can be difficult when the self-interest of each respective group differs, but the ultimate goal of helping animals as much as possible should unify this.

Perhaps the greatest strength of shareholder activism is that it offers a much more certain path to speaking with company executives. Shareholder activism can automatically get you much closer to these decision-makers, as long as rules and regulations are followed and the resolution is reasonable enough. Other campaigns might only achieve this as the end result of much more extensive activism.

Overall, the literature consistently finds significant positive effects from shareholder activism.

Naaraayanan et al. (2020) is particularly interesting as perhaps the only direct material test of shareholder activism. That is, it tests for the underlying improvement of interest (in this case, improvement in environmental outcomes), rather than intermediate variables such as company agreement to the reforms.

It studies the impacts of environmental shareholder activism by examining the material consequences of these campaigns. They analyse whether there are improvements in air quality within a 1 mile radius of plants of companies targeted by these campaigns. They find that the average reduction in pollution by targeted firms is 13%.

They also note that recent reforms have granted shareholders more rights, which are likely to make future shareholder activism more effective, though they conclude that further research is required to pinpoint exactly how much value is created through shareholder campaigns.

In contrast, Weinstein de Wied and Richtor (2019) note that while shareholder activism does guarantee “a seat at the table” and a “voice on the board” there is certainly no guarantee that shareholder activism will either necessarily succeed or revolutionise the company if successful.

Kölbel et al. (2019) analyse four empirical studies assessing company engagement with shareholder requests and find “direct evidence that investors can affect companies through shareholder engagement, especially when the costs of demanded reforms are low, investors wield influence, and companies have prior experience with engagement”. These studies say analyse as part of the review are described in the following table from the review:

Of these, Barko et al. (2022) and Dyck et al. (2019) find that shareholder proposals are associated with increases in ESG ratings of the targeted companies, providing evidence of reforms detected by the external evaluation of the ESG rating.

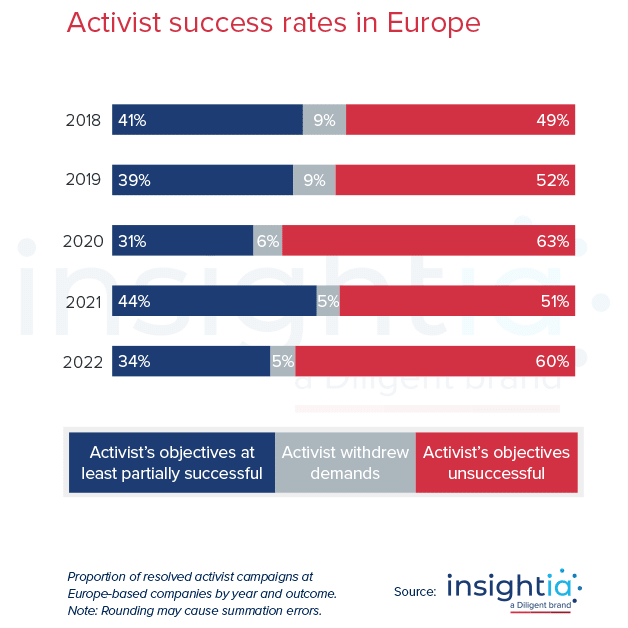

Insignia, an organisation that provides information on shareholder activism produces an annual report that includes statistics on success rates of shareholder activism. Figure 1 below in their 2023 report also shows success rates of shareholder activism over the last five years.

Figure 1 (Insightia and Wolosky 2023)

It seems to show a slight decrease in the success rate of shareholder activism, with 75% of those demands at least partially satisfied in 2014, as were 67% of demands in 2013 (Interest 2015). We should note that if a proposal is unsuccessful, it does not mean it completely fails to achieve social change (Hallaj 2013).

Some literature, discussed by Kölbel et al. (2019), also addresses which specific factors in shareholder activism are predictive of success. It is important to consider these factors in order to consider the effectiveness of these efforts and how future efforts could be more effective.

Shareholder activism campaigns rely on 1) some level of background public support for the reform in question or 2) some other financial or reputational advantage to the company.

Pure moral motivation for reform without significant public support might occasionally happen, but we think this is less likely.

It may be more difficult for animal advocacy shareholder campaigns to get this kind of support as compared with causes with greater public limelight such as climate change (sbehmer 2022).

Kölbel et al. (2019) find that requests in the environmental focused requests have lower success rates than social requests. They find that the most important underlying variables here may be the cost of the reforms in question. Since there are many welfare reforms that would have a large effect on animal welfare well-being inexpensive[4], this could be to the advantage of animal welfare shareholder activism.

Below is a list of some of the main organisations and individuals engaged in shareholder activism relating to animal advocacy or to generally improving practices surrounding animal agriculture (such as environmental or human health concerns):

The overall number of animal activism shareholder proposals is relatively small. Hallaj (2013) reviews animal activism shareholder campaigns prior to the publication date of 2013. They note that the number of shareholder campaigns pursued by the movement has decreased by over 50% from a peak of 37 in 2010 to only approximately 15 proposals in each of 2013 and 2014.

Shareholder relativism is disproportionately a US and, to a lesser extent, European phenomenon. In 2018, it was found that 60% of the total of 250 shareholder actions in the year were conducted against US companies, 25% were conducted against European companies and 10% were conducted against Asia-Pacific companies (Weinstein, de Wied, and Richter 2019).

This suggests that shareholder activism in other regions is neglected, though note that to some extent this simply reflects the relative strength of the US economy. Fortunately, advocacy against groups in the US or other Western countries can also improve welfare in other regions involved in the supply chain. For example, World Animal Protection led a shareholder activist campaign against Tesco (a British company) for sourcing pigs from farms in Thailand that use gestation crates (which have been banned in the UK since 1999) (World Animal Protection 2019).

Further, most companies outside of the US have shareholder protection laws that are much worse for shareholder activism, though of course this varies (expert interviews). For example, the UK, which tends to have worse shareholder rights than the US, requires either 5% of total shares of the company or £10,000 pooled across a large number of different shareholders, both of which are typically more difficult to achieve (Fronda 2023).

Siems (2008) finds that developed countries in general have stronger shareholder productions than developing countries. Additionally, they find that shareholder productions have been increasing over the years. Though, as an analysis of 20 countries from 1995 to 2005, their sample is limited.

There is no option for shareholder resolutions in most Asian countries, except for Japan (expert interviews), but some other softer mechanisms are available such as participating in shareholder meetings, private discussions with the board, and talking to other shareholders to garner support (CFA Institute 2010).

In many countries in Asia, there are fewer automatic rights associated with shareholder ownership and confrontational approaches risk significant backlash. Additionally, shareholders and the board of directors may be less aware of and responsive to ethical issues surrounding the farming of animals. Shareholder activism does of course happen in Asia, but it tends to happen in a non-adversarial and more cooperative way, especially in more authoritarian countries (CFA Institute 2010).

There may be structural impediments to conducting shareholder activism in emerging markets, but it may also be easier to find “win-win” solutions (those that are both profitable and improve animal welfare) because of the relative inefficiency and underdeveloped nature of those markets (Weinstein, de Wied, and Richter 2019). This can in turn be used as a point of leverage to advocate for those reforms. These issues are reflected in far fewer settlements in some regions, such as Asia, with efforts in the US being much more successful.

(Insightia and Wolosky 2023)

The successes of shareholder activism have also tended to be quite top-heavy with three shareholder activist entities being responsible for 70% of board seats won by shareholder activist campaigns in 2018 (Weinstein, de Wied, and Richter 2019).

Here we examine some cases of shareholder activism both in the context of animal advocacy and outside of it.

Carl Icahn is a billionaire investor who is known for a strategy of shareholder activism against underperforming companies in order to generate profit. He was noted as the second largest activist investor in the world according to his activity in 2022 (Insightia and Wolosky 2023). However, in part because of the influence of his daughter who has worked at the Humane Society of the United States (HSUS) (Torrella 2022), he has also leveraged his shareholder’s experience and investment resources towards animal welfare reforms.

In 2012, an alliance of Carl Icahn and HSUS put pressure on McDonald’s to stop supplying from producers that continued to use gestation crates for pregnant pigs. This proposal appeared to be successful as of 2012 when McDonald’s committed to ending gestation crates for pregnant sows by 2022. However, as the proposed date approached, it soon became clear that Mcdonald’s did not intend to follow through with this commitment (Torrella 2022).

This prompted a proxy fight by Carl Icahn to push McDonald’s to stop supplying from all producers using gestation crates globally by 2024. This effort was ultimately unsuccessful with only 1% of shareholders voting in favour of the board member suggestions put forward by Carl Icahn (BBC News 2022). Following the loss, Icahn also dropped a proposed proxy fight against Kroger Co. also concerning gestation crates for pregnant pigs (Reuters 2022).

It is unfortunate that the series of shareholder activism campaigns was not ultimately successful. Though it is surprising Carl Icahn was not able to achieve more, we should note that in this case Carl Icahn owned only 200 shares in McDonald’s, worth approximately $50,000 USD, so this was a very small investment by his standards (Helmore 2022).

One anonymous investor in the case claims that the case may have failed because Carl Icahn did not make any mention of how the reforms would contribute to long-term shareholder value (Insightia and Wolosky 2023). This is a very surprising oversight if accurate.

Shareholder activism against companies operating in apartheid era South Africa is perhaps the earliest case of shareholder activism. It had been allowed since the 1930s, but had not yet been employed for social change in this way (Behar 2016). This started with a resolution put forward in 1971 for General Motors to end discriminatory practices in South Africa.

The resolution was resisted with General Motors following a defensive strategy with only some reforms between 1971 and 1976 (Malone and Roberts 1994). However, social awareness of the issues increased putting more pressure on all companies operating in South Africa. Public relations blunders surrounding this soon caused a public relations nightmare for General Motors, perhaps driving eventual change at the company.

The resolution was eventually passed in the form of the Sullivan Principles (viewable here). These were a series of, progressive for the time, reforms that were supposed to lead to the end of apartheid in South Africa within 10 years. Additionally, by 1986, four additional principles had been added.[5] Perhaps under the influence of the Sullivan Principles, General Motors eventually adopted a desegregated workplace in South Africa. From General Motors, these principles spread to other companies working in South Africa (Behar 2016). 12 major US companies signed up in 1977 with an additional 93 signing in the following year, peaking in 1986 with 183 signatories (Malone and Roberts 1994).

Isolating causality is difficult here. It seems that shareholder activism is responsible for some, but certainly not all of the successes identified here. Companies operating in apartheid era South Africa faced both immense moral pressure from the public to reform or get out, as well as potential or actual restrictions from the US government, which were expected to have a substantial impact on company practices whether or not shareholder activism took place.

Broyles (1998) analyses the overall effect of shareholder activism on the rolling back and abolition of apartheid in South Africa. He argues that shareholder activism was effective in changing corporate policy in this case and that shareholder activism played a significant role in both causing some corporations to cease operations in South Africa and pressuring others to adopt reforms that, while they did not sever all relations, worked against apartheid.

While support for anti-apartheid shareholder resolutions was initially very low, with most receiving less than 10% of the vote during resolutions, Broyles argues that this started the conversation and that support grew steadily over time until majority support was reached. He also suggests that shareholder activism was considerably more effective than these vote shares represent, even in the earlier stages of the anti-apartheid movement.

As one of the earliest cases of shareholder activism, the success of this case should perhaps be less surprising. General Motors did not know how to react to and successfully handle the shareholder resolution against it, and indeed it handled the situation very poorly. We can expect that future shareholder resolutions to be somewhat less effective, as companies learn to effectively adapt to this tactic and counter it (Behar 2016).

The chief value we see coming from shareholder activism is through its influence on the actions of the firm to reform harmful actions and otherwise reduce the suffering of animals. Any effect these actions have on the expected return through investment in the targeted companies is secondary to this. Nevertheless, shareholder activism would be a more sustainable and attractive approach if it ultimately has a beneficial or at least neutral effect on shareholder returns. If this were true, we would expect more people to be interested in engaging in shareholder activism. Additionally, if shareholder activism positively (or even neutrally) affects share valuation, it will be in the interest of firms to acquiesce to shareholder demands on purely financial grounds.

Concerning this question, there are two types of shareholder activism that are sometimes distinguished in the literature. The first is shareholder activism to improve the functioning of the firm principally in order to increase profits, sometimes called financial shareholder activism. For example, if the CEO was performing poorly this form of shareholder activism could be done in order to force the hiring of a new CEO to replace them. The second type of shareholder activism is the type that we are concerned with in this paper, shareholder activism principally motivated for the public good which seeks to improve the moral practice of the company, sometimes called social shareholder activism (Goranova and Ryan 2014). Of course, there may not always be a clear line between these two forms of activism. Immoral practices by companies can often have a strong negative effect on the reputation at some point farther down the line.

Denes et al. (2017) finds that concerning smaller scale shareholder activism, financial shareholder activism is successful in boosting the shareholder returns while social shareholder activism “is associated with insignificant or very small changes in target firm value”. In contrast, they find that larger scale shareholder activism that credibly threatens and engages in proxy fights can lead large-scale changes in valuation averaging 15%.

There are also several reviews of the literature that do not separately analyse these two forms of shareholder activism:

Overall, we expect that shareholder activism for social reasons will often not affect share valuation, though social activism that focuses on particularly problematic issues that are not expensive to fix may well also increase shareholder valuation.

Shareholder activism has shown a great deal of promise in general with inherent strengths, such as an automatic mechanism for being heard and for getting demands met. This contrasts with other methods of advocacy where these must be earned. It has already seen some victories within animal advocacy and has seen very substantial victories in other areas.

We think there is room to expand the use of shareholder activism for animal advocacy purposes, and judge this would be an effective use of resources, though this should be done only in careful coordination with existing groups because of the inherent difficulty and risk associated with it.

Bajzik, Josef, Tomas Havranek, Zuzana Irsova, and Jiri Novak. 2023. “Does Shareholder Activism Create Value? A Meta-Analysis.” https://www.econstor.eu/handle/10419/272232.

Barko, Tamas, Martijn Cremers, and Luc Renneboog. 2022. “Shareholder Engagement on Environmental, Social, and Governance Performance.” Journal of Business Ethics: JBE 180 (2): 777–812.

BBC News. 2022. “McDonald’s Defeats Billionaire Carl Icahn in Vote over Pigs.” BBC, May 26, 2022. https://www.bbc.co.uk/news/business-61596848.

Behar, Andrew. 2016. The Shareholder Action Guide: Unleash Your Hidden Powers to Hold Corporations Accountable. Berrett-Koehler Publishers.

Broyles, Philip A. 1998. “THE IMPACT OF SHAREHOLDER ACTIVISM ON CORPORATE INVOLVEMENT IN SOUTH AFRICA DURING THE REAGAN ERA.” International Review Of Modern Sociology 28 (1): 1–19.

CFA Institute. 2010. “Shareholder Rights in Asia: Are Shareholders Flexing Their Muscles to Protect Themselves?” CFA Institute.

Chen, James. n.d. “What Is an Activist Shareholder? What They Do and How They Work.” Accessed January 13, 2024. https://www.investopedia.com/terms/s/shareholderactivist.asp.

Denes, Matthew R., Jonathan M. Karpoff, and Victoria B. McWilliams. 2017. “Thirty Years of Shareholder Activism: A Survey of Empirical Research.” Journal of Corporate Finance 44 (June): 405–24.

Dimson, Elroy, Oğuzhan Karakaş, and Xi Li. 2015. “Active Ownership.” The Review of Financial Studies 28 (12): 3225–68.

Dyck, Alexander, Karl V. Lins, Lukas Roth, and Hannes F. Wagner. 2019. “Do Institutional Investors Drive Corporate Social Responsibility? International Evidence.” Journal of Financial Economics 131 (3): 693–714.

Ellis, Kirkland And. 2023. “Shareholder Activism: Lessons from the First Season of Universal Proxy.” Kirkland and Ellis. 2023. https://www.kirkland.com/publications/kirkland-manda-update/2023/06/shareholder-activism-lessons-from-the-first-season-of-universal-proxy.

Ertimur, Yonca, Fabrizio Ferri, and Stephen R. Stubben. 2010. “Board of Directors’ Responsiveness to Shareholders: Evidence from Shareholder Proposals.” Journal of Corporate Finance 16 (1): 53–72.

Ferri, Fabrizio. 2015. “‘low-Cost’ Shareholder Activism: A Review of the Evidence.” Research Handbook on the Economics of Corporate Law. Cheltenham, England: Edward Elgar Publishing. https://doi.org/10.4337/9781781005217.00018.

Goranova, Maria, and Lori Verstegen Ryan. 2014. “Shareholder Activism: A Multidisciplinary Review.” Journal of Management 40 (5): 1230–68.

Hallaj, Summer M. 2013. “A Decent Proposal: How Animal Welfare Organizations Have Utilized Shareholder Proposals to Achieve Greater Protection for Animals.” The John Marshall Law Review 47: 795.

Harsh, Cameron. 2020. “Shareholder Advocacy as a Tool for Change.” World Animal Protection. June 24, 2020. https://www.worldanimalprotection.us/blogs/shareholder-advocacy-tool-change.

Helmore, Edward. 2022. “Carl Icahn Pressuring McDonald’s to Improve Welfare of Pigs Raised for Meat.” The Guardian, February 22, 2022. https://www.theguardian.com/business/2022/feb/22/carl-icahn-pressuring-mcdonalds-improve-welfare-pigs.

ICCR. 2023. “Shareholder Resolutions.” Interfaith Center on Corporate Responsibility - ICCR Builds a More Just and Sustainable World by Integrating Social Values into Corporate and Investor Actions. ICCR. July 14, 2023. https://www.iccr.org/shareholder-resolutions/.

Insightia, and Olshan Frome Wolosky. 2023. “The Shareholder Activism Annual Review.” Insightia. https://docs.insightia.com/issues/2023_02_16_Insightia_SAAR2023.pdf.

Interest, Carried. 2015. “Activist Investor Definition.” Carried Interest. June 29, 2015. https://web.archive.org/web/20190625230601/https://www.carriedin.com/activist-investor.

Kölbel, Julian F., Florian Heeb, Falko Paetzold, and Timo Busch. 2019. “Can Sustainable Investing Save the World? Reviewing the Mechanisms of Investor Impact.” https://doi.org/10.2139/ssrn.3289544.

Levin, Michael R. 2022. “The Cost of Proxy Contests.” The Harvard Law School Forum on Corporate Governance. The Harvard Law School Forum on Corporate Governance. May 25, 2022. https://corpgov.law.harvard.edu/2022/05/25/the-cost-of-proxy-contests/.

Malone, David, and Robin W. Roberts. 1994. “An Analysis of Public Interest Reporting: The Case of General Motors in South Africa.” Business & Professional Ethics Journal 13 (3): 71–92.

Naaraayanan, S. Lakshmi, Kunal Sachdeva, and Varun Sharma. 2020. “The Real Effects of Environmental Activist Investing.” https://doi.org/10.2139/ssrn.3483692.

Odene, Amy, and James Ozden. n.d. “Josh Balk on Using Shareholder Activism to Win Change from the World’s Largest Food Companies.” How I Learned to Love Shrimp Podcast. Accessed January 13, 2024. https://www.howilearnedtoloveshrimp.com/podcast/episode/7d321dc0/josh-balk-on-using-shareholder-activism-to-win-change-from-the-worlds-largest-food-companies.

Rafaqat, Simon, Sana Rafaqat, Sahil Rafaqat, Saoul Rafaqat, and Dawood Rafaqat. 2022. “Shareholder Activism and Firm Performance: A Review.” Journal of Economics and Behavioral Studies 14 (4(J)): 31–41.

Reuters. 2022. “Carl Icahn Drops Proxy Fight against Kroger after McDonald’s Defeat.” Reuters, June 6, 2022. https://www.reuters.com/business/retail-consumer/carl-icahn-drops-proxy-fight-against-kroger-withdraws-nominees-2022-06-06/.

sbehmer. 2022. “Shareholder Activism.” Effective Altruism Forum. 2022. https://forum.effectivealtruism.org/posts/fqf4vgCWebTszvHm9/shareholder-activism.

“Shareholder Advocacy as a Tool for Change.” 2020. World Animal Protection. June 24, 2020. https://www.worldanimalprotection.us/blogs/shareholder-advocacy-tool-change.

“Shareholder Campaigns.” 2010. PETA. June 23, 2010. https://www.peta.org/issues/animals-used-for-experimentation/shareholder-campaigns/.

Siems, M. 2008. “Shareholder Protection around the World (’leximetric II').” Corporate Law: Corporate & Financial Law: Interdisciplinary Approaches eJournal, March. https://doi.org/10.2139/ssrn.991092.

Sjöström, Emma. 2008. “Shareholder Activism for Corporate Social Responsibility: What Do We Know?” Sustainable Development 16 (3): 141–54.

Torrella, Kenny. 2022. “The Corporate Raider Taking Aim at McDonald’s over the Treatment of Pigs.” March 3, 2022. https://www.vox.com/future-perfect/22958698/mcdonalds-icahn-pork-pigs-gestation-crates-animal-welfare.

USSIF. n.d. “Shareholder Resolutions.” The Sustainable Investment Forum. Accessed January 24, 2024. https://www.ussif.org/resolutions.

Weinstein, Gail, Warren S. de Wied, and Philip Richter. 2019. “The Road Ahead for Shareholder Activism.” Harvard Law School Forum on Corporate Governance and Financial Regulation. https://corpgov.law.harvard.edu/2019/02/13/the-road-ahead-for-shareholder-activism/.

World Animal Protection. 2019. “We Spoke up for Mother Pigs at Tesco’s Annual General Meeting.” World Animal Protection. November 6, 2019. https://www.worldanimalprotection.org.uk/news/we-spoke-mother-pigs-tescos-annual-general-meeting.

We use the term ‘shareholder activism’ in this report, though the term ‘shareholder advocacy’ is also often used in the literature. These terms are used fairly interchangeably and are used to describe a wide variety of shareholder action, including both socially and financially motivated advocacy or activism.

The exact rules around shareholder advocacy will vary by jurisdiction, but tend to have broad similarities. This article will discuss the US rules as default, but note that this should be adapted to the jurisdiction in question.

ESG stands for Environmental, Social, and Governance. ESG ratings represent an attempt to rank investments according to the company's ethical performance in these areas, and so investors choose more ethical investments.

See for example production cost increases of between 1 to 3% for stunning fish before slaughter in Italy. Other reforms are more expensive, such as an estimated increase of 5 to 16% for cage free egg production, though note that these reforms are also expected to bring some financial benefits to the company.

The additional four principles read as follows:

“To support the unrestricted rights of black businesses to locate in urban areas of South Africa.

To influence other companies in South Africa to adhere to standards propound equal rights in their operations.

To support the mobility of black workers in all respects.

To support the ending of all laws that constitute the structure of apartheid.” (Malone and Roberts 1994)

“To support the unrestricted rights of black businesses to locate in urban areas of South Africa.

To influence other companies in South Africa to adhere to standards propound equal rights in their operations.

To support the mobility of black workers in all respects.

To support the ending of all laws that constitute the structure of apartheid.” (Malone and Roberts 1994)

Executive summary: Shareholder activism has shown promise as an effective advocacy tool for animal welfare causes, with some successes already, and opportunities exist to expand its use if done carefully in coordination with existing groups.

Key points:

This comment was auto-generated by the EA Forum Team. Feel free to point out issues with this summary by replying to the comment, and contact us if you have feedback.