Comments

Most consumers value animal welfare. According to most people, the cost of animal suffering in the production of animal-based food, is huge. In monetary terms, the suffering of most broiler chickens would correspond to 8000 euros per kilogram of chicken meat. This external cost of animal suffering is much higher than the external costs of e.g. environmental impacts, public health risks or climate change. Of course, an animal welfare levy of 8000 euros per kilogram chicken meat would immediately wipe out the entire meat production sector, and would not be politically feasible. There is a related but much more feasible proposal for the food retail and services sectors (supermarkets, restaurants,…), that is likely to have a wide support: an internal animal welfare feebate.

A feebate is a combination of a fee and a rebate. In the proposal, the fee is an animal welfare levy or tax on products that involve animal suffering, such as meat, and the rebate is a subsidy for animal-free (plant-based) alternatives. An internal feebate means that the feebate is applied not by a government at the national level, but internally by a food retail or service business at the company level. Supermarkets or restaurants sell animal products at a price higher than the production costs and use the extra revenue to cover the losses of selling plant-based meat alternatives at a price below the production costs.

In more detail, the most feasible proposal consists of a 2 to 3 euro per kilogram levy on products from animals smaller than a pig (in particular chicken meat, eggs, fish and shrimp), and a subsidy on the best (tastiest, healthiest) plant-based meat alternatives (in particular plant-based chicken fillet and nuggets), with a subsidy cap such that the meat alternatives do not become cheaper than their untaxed animal-based counterparts (i.e. the price of the plant-based alternatives cannot fall below the current, baseline price of chicken meat).

This proposal should be feasible, because:

- according to a survey (in Belgium), the majority of people are willing to pay a 3 eur/kg animal welfare levy on meat,

- according to large blind taste tests, a majority of consumers think that some plant-based chicken(less) fillet and nuggets taste at least as good as their animal-based counterparts (chicken fillet and chicken nuggets),

- most of the subsidized plant-based chicken meat alternatives have a similar or better nutritional value than chicken meat: they contain essential protein, minerals and vitamins as in chicken meat, and additionally contain more healthy fibres than chicken meat),

- according to a rough calculation (see addendum below), the revenue from a 2€/kg welfare levy on chicken meat can probably finance a subsidy for plant-based fillet and nuggets such that those plant-based products can be sold at the current price of (untaxed) chicken meat, which means that consumers keep the option to buy a product that is at least as tasty, healthy and cheap as current chicken meat,

- the feebate can be applied at the level of a company and doesn’t require a new tax law, nor extra governmental administration and control,

- only the animal products that have by far the highest welfare footprints (i.e. the most animal suffering) are taxed,

- the feebate has additional environmental benefits (plant-based meat alternatives have a lower environmental footprint than animal-based counterparts) and public health benefits (plant-based meat alternatives do not increase the risk of infectious zoonotic diseases), such that the feebate fits within corporate social responsibility and Environmental, Social and Governance (ESG) policy,

- the subsidy cap ensures that the system is stable (without the cap, the price of subsidized plant-based alternatives may become zero, consumers may completely shift towards the free plant-based alternatives, the animal-based products market may completely collapse and hence there will no longer be any tax revenues to finance the subsidy).

With this proposal, the quantity of chicken meat could decrease with about a quarter. As most farmed animal suffering is due to the suffering of chickens, this proposal could potentially decrease farmed animal suffering with more than 20%.

Addendum

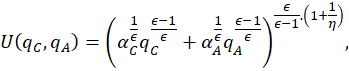

To measure the economic impact of a feebate on chicken meat, we can start with a consumer’s utility function with a constant elasticity of substitution (CES):

with

the consumed quantity of meat, in particular chicken fillet,

the consumed quantity of plant-based meat alternatives, in particular chicken(less) fillet,

the elasticity of substitution (due to lack of estimates in the economics literature, I assume this parameter to be equal to 2 for ease of calculations),

the price elasticity of demand (assumed to be equal to -0,7, according to a systematic review),

and

the non-monetary preferences for resp. chicken meat and alternatives, representing taste preferences, food culture, cooking habits and familiarity.

The current prices for chicken fillet and alternatives are respectively

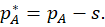

Introduce an animal welfare tax

and

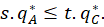

As the subsidy is financed by the tax, we have the budget constraint:

Here,

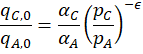

the non-monetary preferences can be calculated to be

To calculate how much chicken meat is reduced due to the feebate, we can express the equilibrium quantity as

with

the aggregated price index in the feebate system and

There are two operational phases:

- the budget-balanced phase whereby the tax revenue matches the total subsidy payout,

- the fiscal surplus phase, when the tax revenue is higher than the total subsidy.

The threshold between the two phases lies at a tax rate of 1,17 eur/kg.

In the fiscal surplus phase, the excess tax revenue can be used to subsidize the price of other plant-based alternatives of animal products. The table below summarizes the results.

| Tax rate (eur/kg) | Chicken fillet price (eur) | Alternative plant-based fillet price (eur) | Chicken fillet quantity bought relative to baseline | System phase |

|---|---|---|---|---|

| 0 | 9 | 23 | 100% | Baseline (no policy) |

| 0,5 | 9,5 | 16,2 | 95% | Budget balanced |

| 1,17 | 10,17 | 9 | 87% | Cap threshold |

| 2 | 11 | 9 | 79% | Fiscal surplus |

| 3 | 12 | 9 | 70% | Fiscal surplus |

At a tax rate of 2 eur/kg, the quantity of chicken fillet decreases with 21% and the plant-based fillet price equals the baseline chicken fillet price.

Note that in this example, the plant-based alternative (fillet that tastes as least as good as chicken fillet) has a very high baseline price: 250% times the price of chicken fillet. Even with such a large price gap between the animal-based and plant-based products, a relatively moderate tax rate of 2 eur/kg could drop the price of the subsidized alternative to the baseline (untaxed) price of the animal product.

When the elasticity of substitution becomes higher than 2,5, or the current market share of plant-based fillet would be higher than 2%, the threshold tax rate would be above 3 eur/kg. In that case, a tax rate below 3 eur/kg would not suffice to drop the price of the plant-based product to the baseline price of the animal product. As both the prices of the animal product and its plant-based alternative are higher than the untaxed price of the animal product, consumers are no longer able to by a product that is as cheap as the current animal product.