We should be interested in telehealth interventions, especially for non-communicable diseases, or in countries that’re rapidly connecting to the internet. Not only because they’re lower-cost per person, but because they unlock much faster & greater scale.

BetterHelp is the most-used teletherapy platform in the world, and are owned by Teladoc, the largest telehealth company. Their users are matched to a licensed counsellor on-demand, who they can text at-will and schedule calls with, for a monthly fee between US$260–400. As such, I think it makes an interesting case study in what the characteristics of telehealth scale look like. In this post, I’ll argue that they’ve saturated their addressable market in the U.S., which can provide us clues for the limits of scale in other markets, such as India or Latin America.

Note: I’ll treat BetterHelp as essentially U.S.-only for now

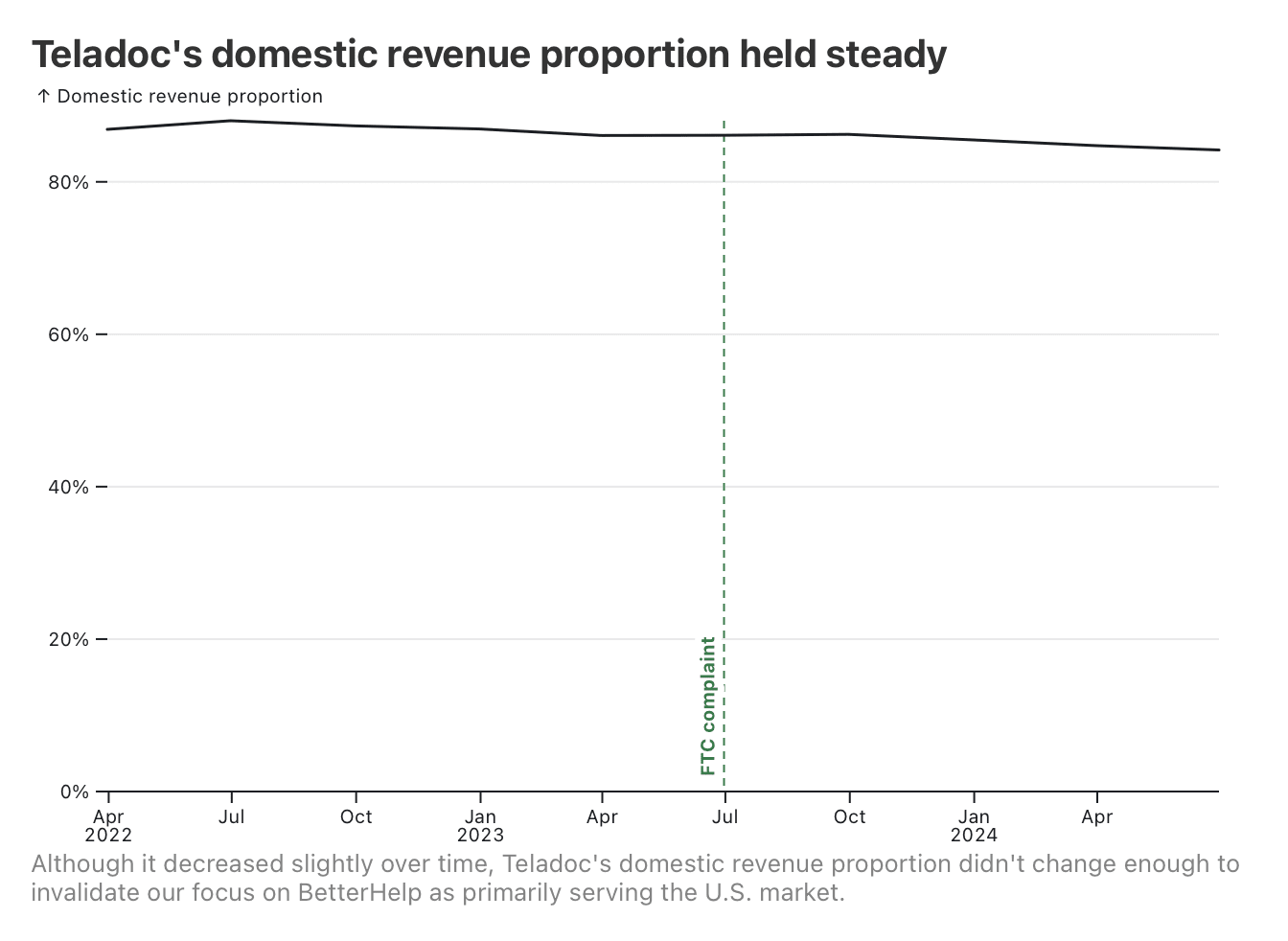

In 2023, the FTC filed a complaint about BetterHelp, for sharing diagnosis information with Facebook and Snapchat for the purposes of advertising, after claiming they wouldn’t. In the final complaint, issued July 2023, they note that BetterHelp has over 374,000 active U.S. users, and a contemporaneous earnings release notes they have 476,000 total active users, for a proportion of 78.57%.

In that same earnings release, Teladoc’s U.S. revenue makes up 86.11% of their total revenue—this holds steady over time, at 86.88% in Q1 ’22, and 84.12% in Q2 ’24. BetterHelp have mentioned their international business “is in the mid-teens” as a percentage of their total, and BetterHelp makes up 41.25% of Teladoc’s revenue, so it’s not unreasonable to assume that the proportions are similar.

In response to falling user numbers, BetterHelp are pursuing international expansion, but this increase hasn’t shown up in the numbers yet. So, when discussing market saturation, I’ll be referring only to the U.S.

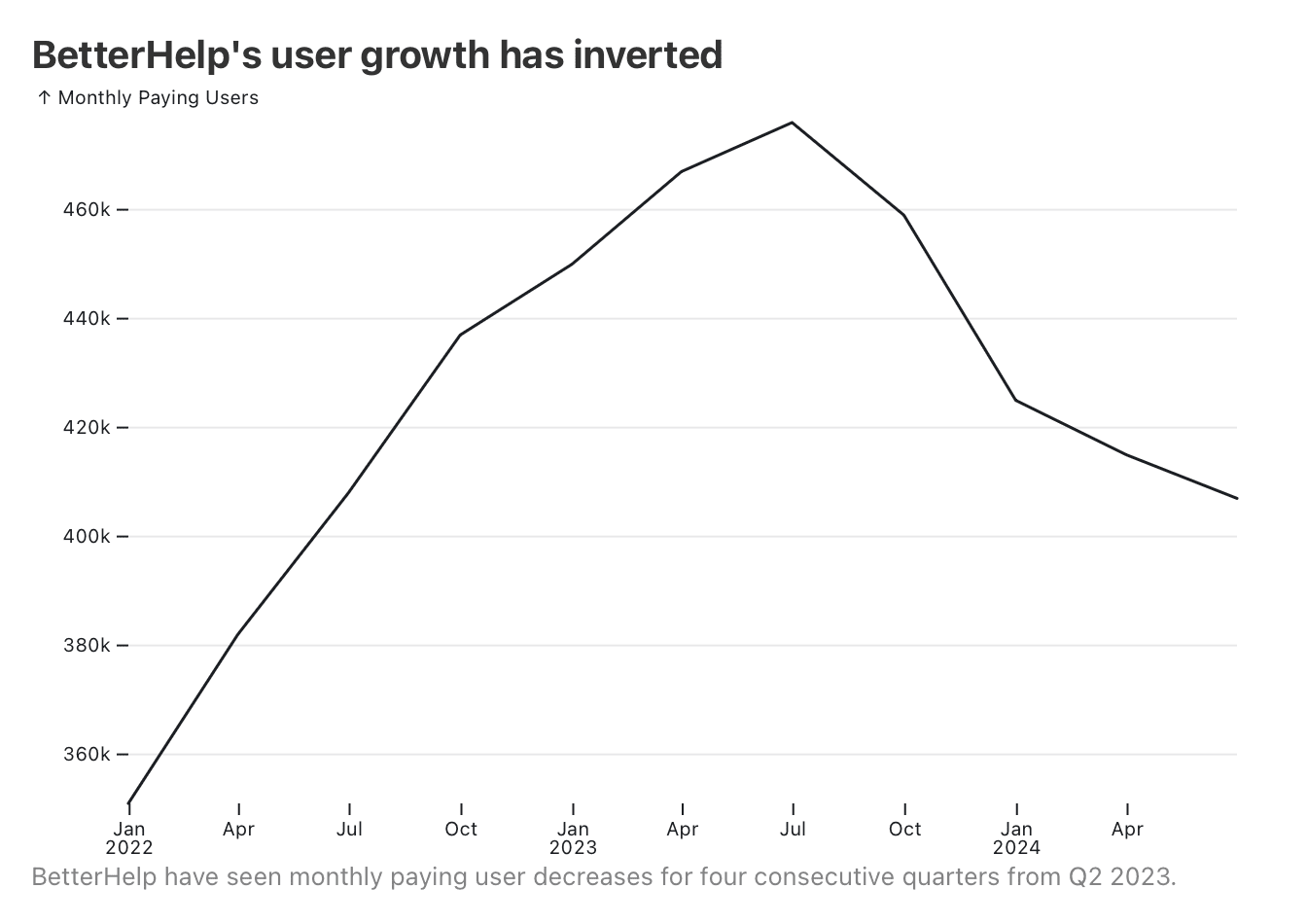

BetterHelp’s user growth has inverted

Here’s BetterHelp’s reported average monthly paying users (reported quarterly), since they started publicly reporting the data in their financials.

Not only have they stopped adding new paying users, but the number of paying users is decreasing. Let’s investigate what’s happening, and hopefully we can understand why.

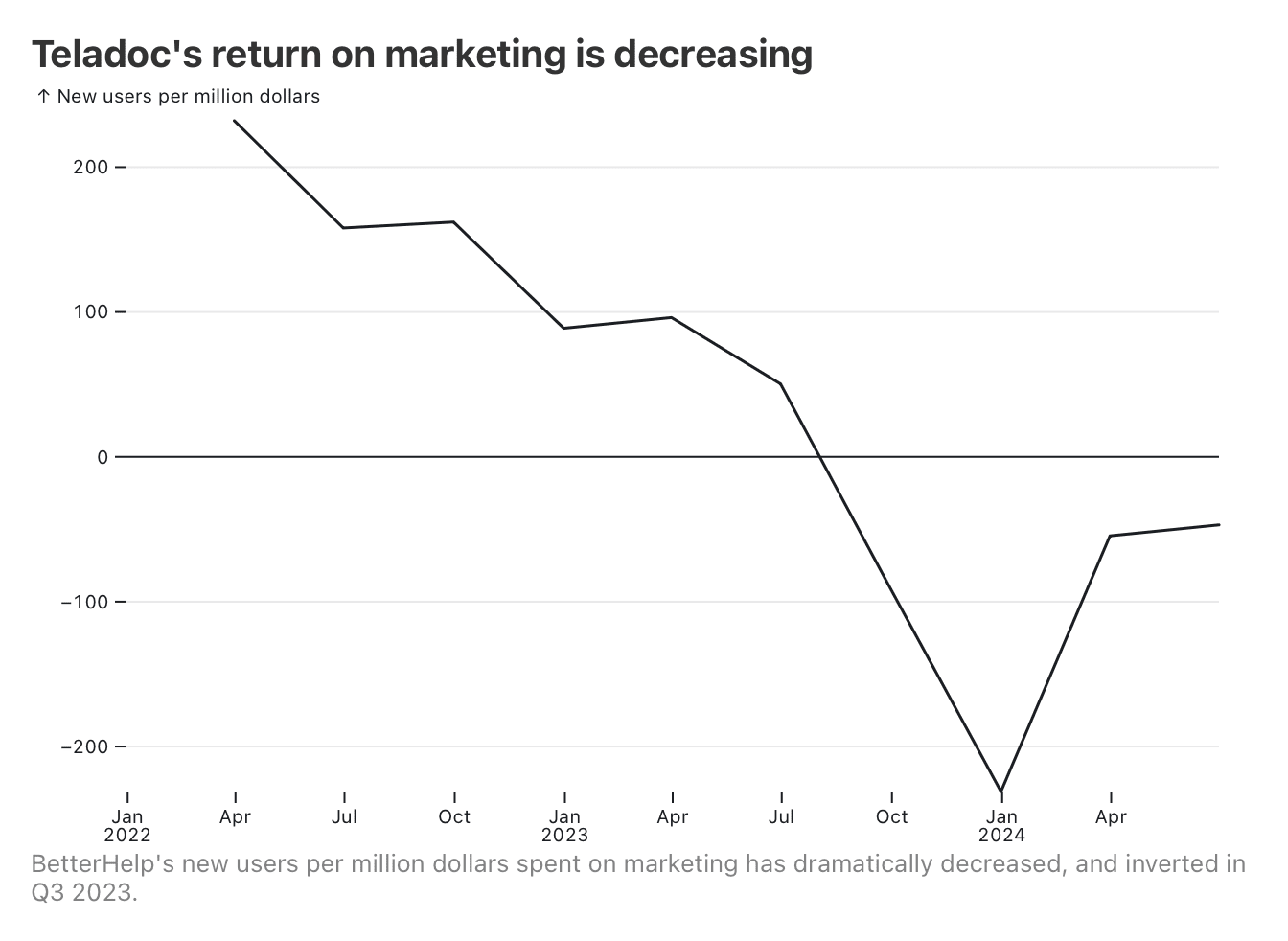

The same ad spend is returning less growth

Teladoc don’t split out their marketing expenses by business unit, but whenever their ad spend increases, they “substantially” attribute the increase to BetterHelp. Because BetterHelp is their only direct-to-consumer business, we can assume almost all of Teladoc’s marketing spend is spent on BetterHelp. We can see that, although user numbers have decreased, ad spend remains stable, leading to apparent losses on marketing.

Increasing customer acquisition costs are a strong indicator of a saturated market. In their Q2 ’24 earnings call, CFO Mala Murthy notes:

BetterHelp growth is dependent on our ability to efficiently deploy marketing dollars to acquire new customers. Our scale makes us the largest advertiser of virtual mental health. And while our spending is diversified across various channels, there is only so much incremental ad spend we can drive in a short period of time without further inflating our customer acquisition costs. At our scale, and at these elevated levels of customer acquisition costs, we are making a conscious decision not to chase inefficient customer acquisition to points below an appropriate return. So, this balanced approach and focus on driving ROI and margin is going to come at a lower overall rate of top-line growth as long as customer acquisition costs in our key advertising channels remain elevated.

Teladoc are struggling to find new users who find their offering acceptable in the U.S. market, despite continuing to spend strongly on advertising. This issue has caused investors to file a class action lawsuit against Teladoc for continuing to grow ad spend in the face of diminishing returns, and may have led to BetterHelp’s and Teladoc’s leadership being replaced.

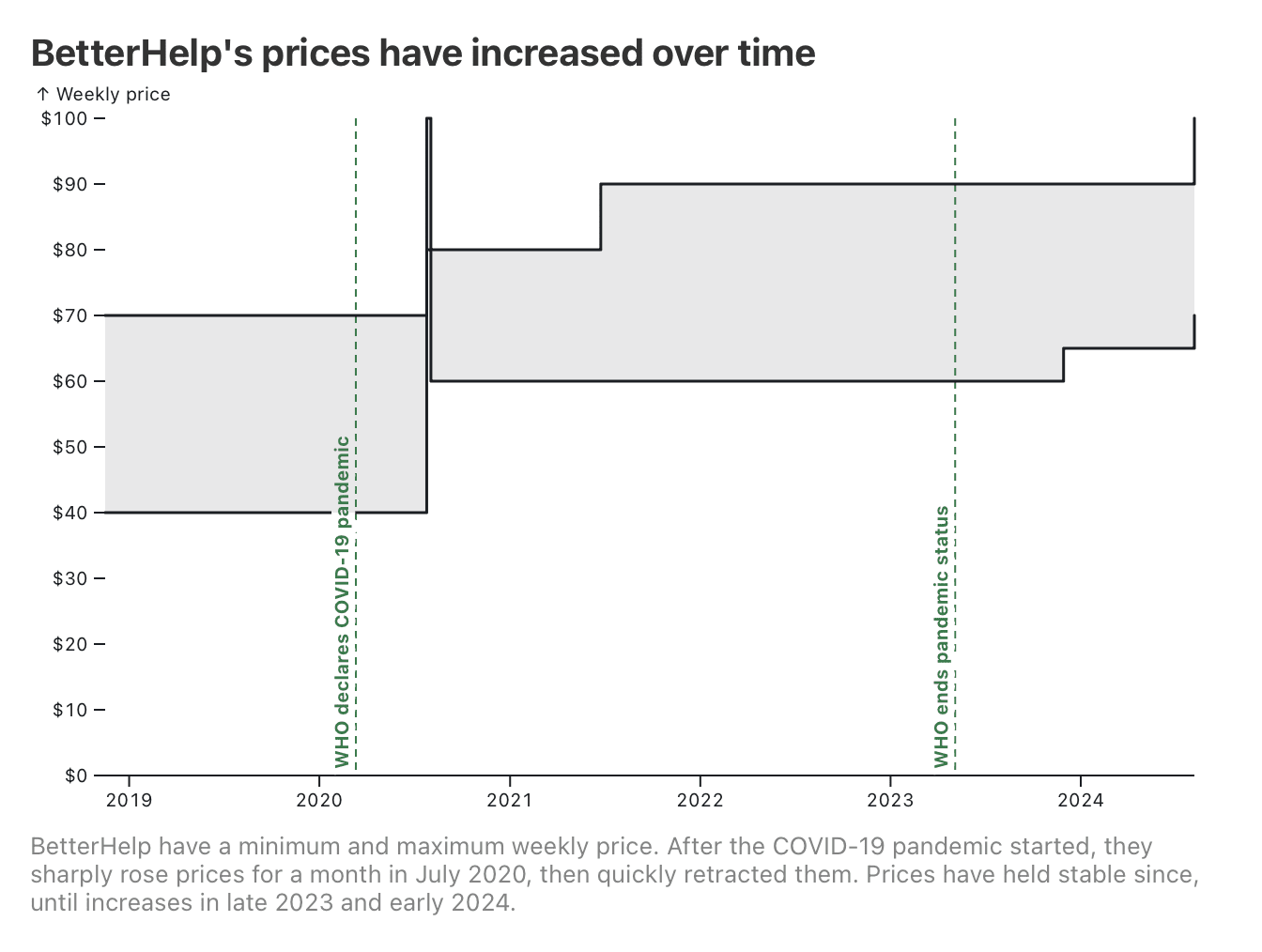

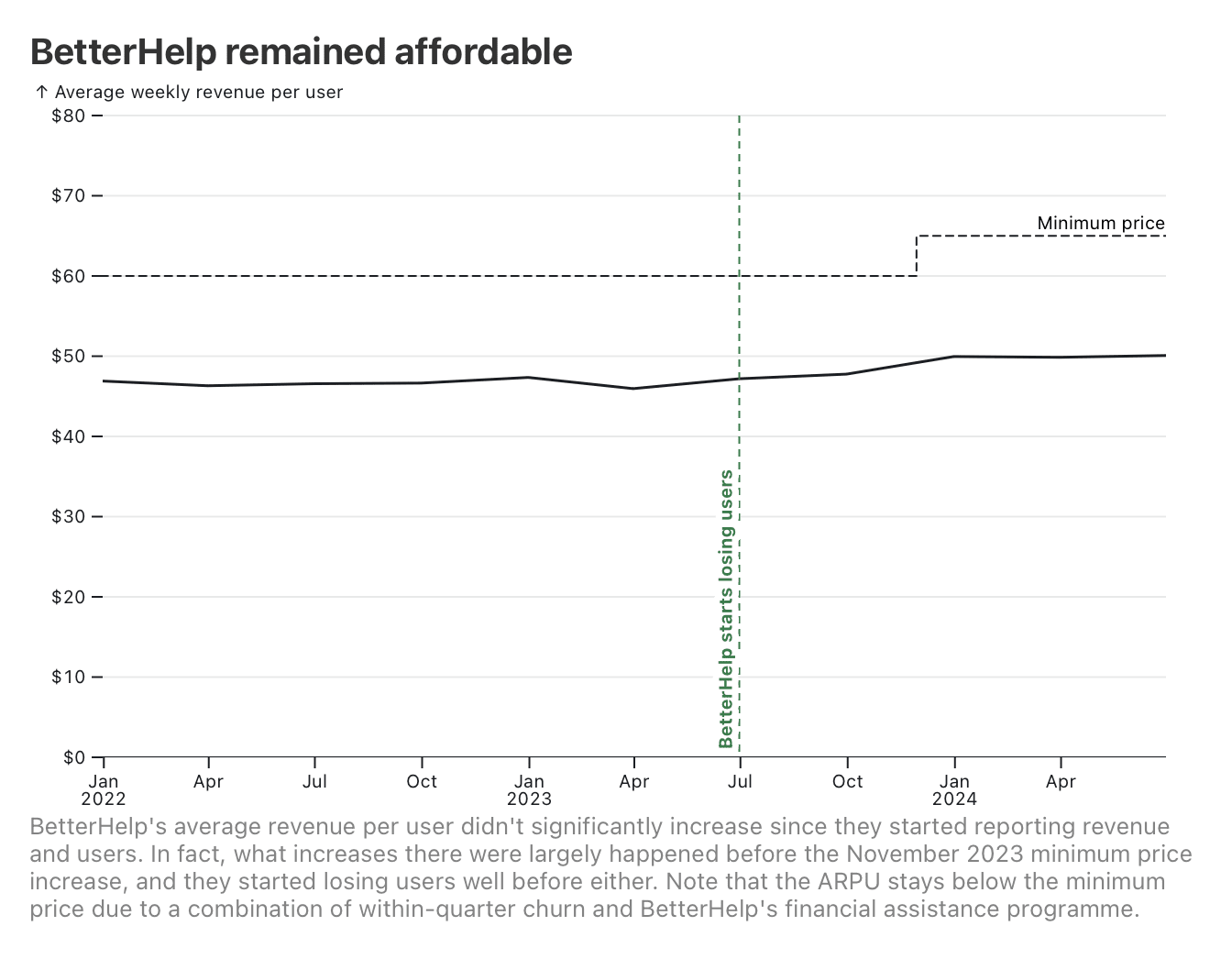

The service didn’t become less affordable

BetterHelp publicly report minimum and maximum prices. We can see those prices over time:

We have revenue and user numbers for BetterHelp since Teladoc started reporting it in Q4 ’21. So, we can calculate the average revenue per user to get a sense of what users are actually paying within those bounds.

BetterHelp’s ARPU over this period has held steady, and, in fact, seems to have increased before the November 2023 minimum price increase (from US$60 → US$65). (I didn’t find evidence that they’d quietly increased prices on existing users before updating their website, either). Notably, they started losing users before either event.

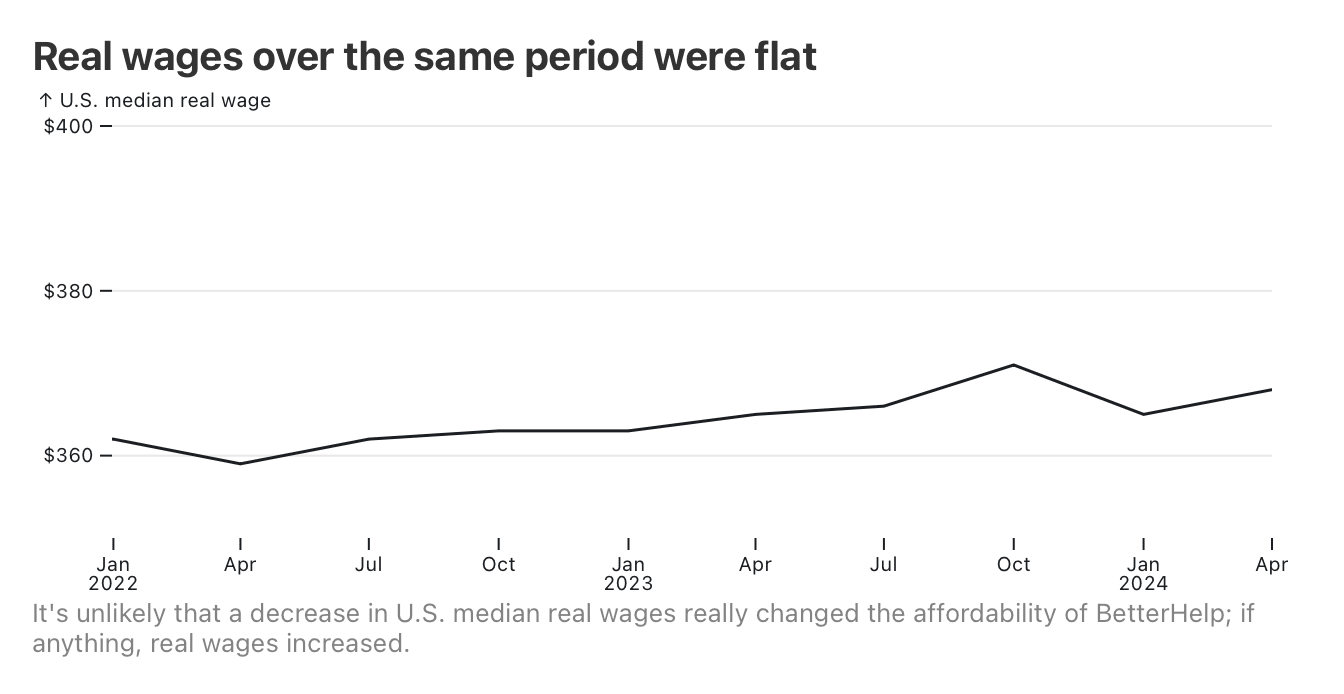

Just to be sure, let’s check that real wages didn’t massively decrease over that time, which would’ve caused users to cut back.

While it’s true that the service did start pulling a higher average revenue per user, and underwent a price increase, these are clearly not the causes of that user churn (although I don’t doubt that they exacerbated it). If anything, it looks as if low-ARPU users churned on their own, causing the ARPU increase, which then meant BetterHelp could raise prices without significant sensitivity.

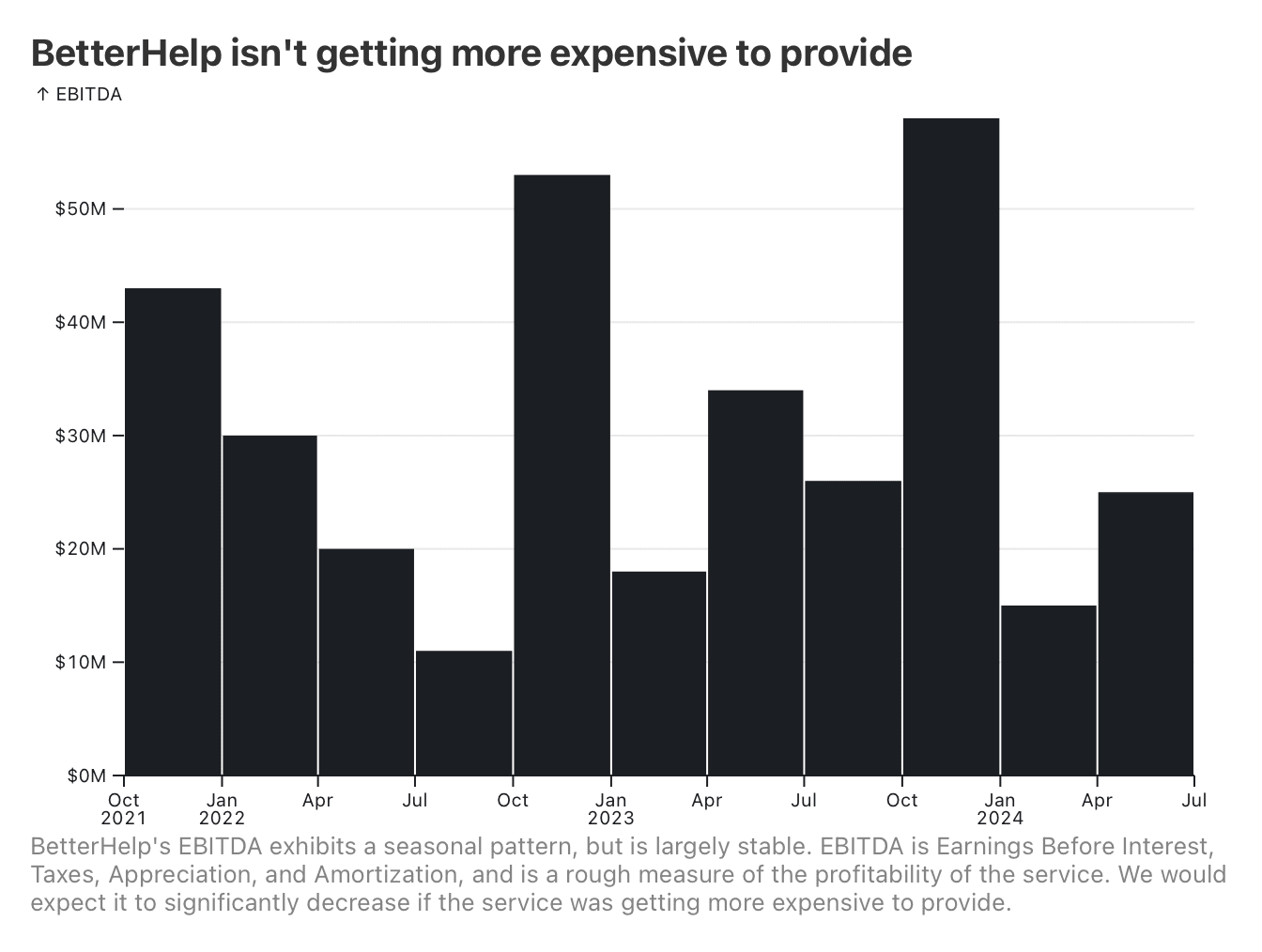

The service isn’t getting more expensive to provide

The recent price increase might also be an indicator that the service is getting more expensive to provide. However, there’s not much in their recent EBITDA to suggest this, as it’s not decreasing over time outside of seasonality.

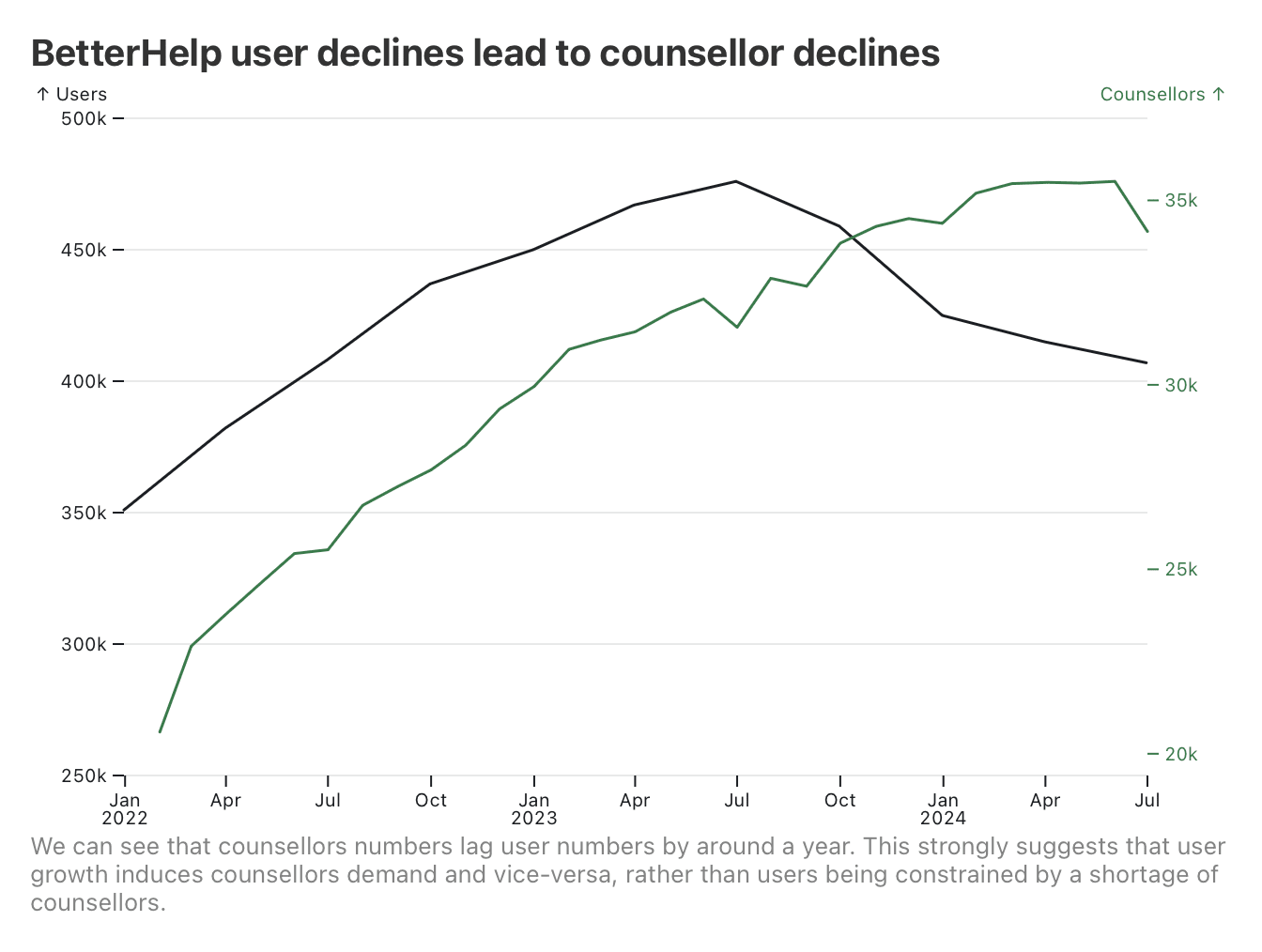

They haven’t run out of counsellors

BetterHelp used to post their number of counsellors on their website, until quite recently (they now only report rough numbers occasionally). We can use the Internet Archive to painstakingly plot this over time, against their reported active user numbers.

It’s clear that, if anything, the number of counsellors lags the number of users. Given that prices and EBITDA have remained relatively stable, it does seem like counsellors that’re losing workloads are leaving the service.

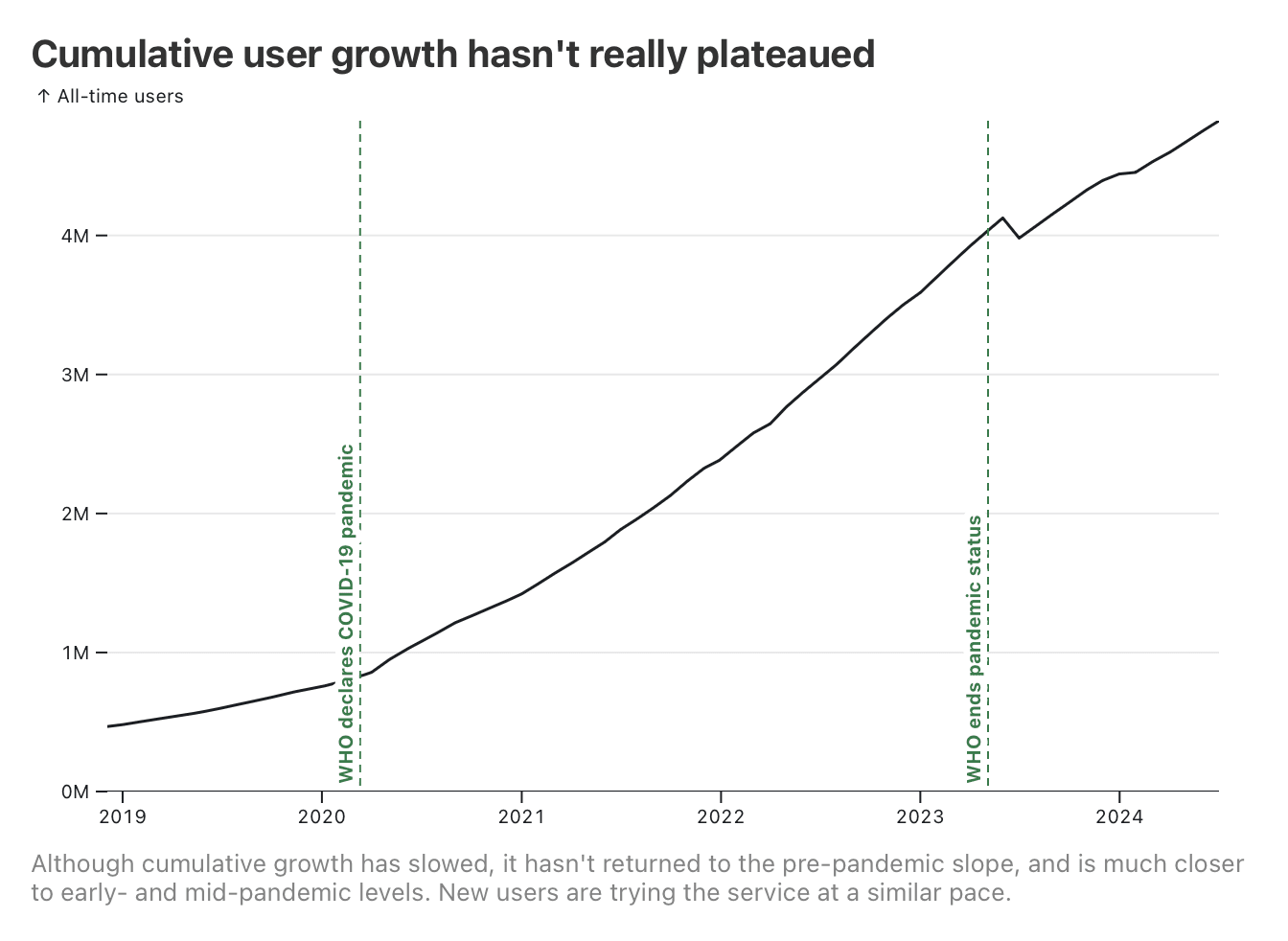

They’re not merely reverting to a pre-pandemic growth rate

BetterHelp also used to post a cumulative count of people who had ever used the service. We can use this to get a sense of their top-of-funnel growth rate (where quarterly paying users is subject to unknown churn rates).

Immediately, it’s clear that the pandemic had an accelerating effect on growth—but that growth rate hasn’t reverted to pre-pandemic levels. It does appear that new users continue to try the service at relatively high rates, but that, as we’ve seen from the active user data, they don’t stick around.

It seems unlikely that their controversies are the main driver

BetterHelp have undergone two significant controversies over this period.

In 2018, they were a prominent YouTube sponsor. It was at this point that the public discovered that their Terms of Service used dodgy legalese to indemnify them if it came to light that one of their counsellors wasn’t credentialed. Although there are very few reports of this happening (BetterHelp do vet their counsellors), it did surface a number of other negative reports from users. This led to prominent campaigns for YouTubers to drop BetterHelp as a sponsor, which presumably caused brand damage. This controversy hasn’t ever really been put to bed, re-emerging periodically on YouTube.

As already alluded to, in July 2023 the FTC filed a complaint against them, for sharing diagnosis information with advertisers, after claiming they wouldn’t. Settlement payments for this began in May 2024.

I think it’s plausible that these trends impacted BetterHelp’s reputation among customers, but this is very hard to measure. The YouTube drama in particular has recurred over a number of years, so it’s not clear where it would show up in the numbers. Nor is it clear whether Teladoc would mention reputation concerns in their earnings as a headwind (FWIW, they haven’t, nor has an analyst even asked about the FTC complaint).

Overall, I think it’s plausible that the controversies turned away some potential users (myself included), but I doubt this is massively reducing their ceiling without more evidence.

BetterHelp are finding higher ad yield outside the U.S.

BetterHelp’s international pricing is the same as the U.S. after currency conversion, and they note that they’re seeing higher ad yields in those markets, justifying an international expansion. Conversely, their previous lack of an international focus indicates that those ad yields weren’t better in the past, implying a recent saturation in the U.S.

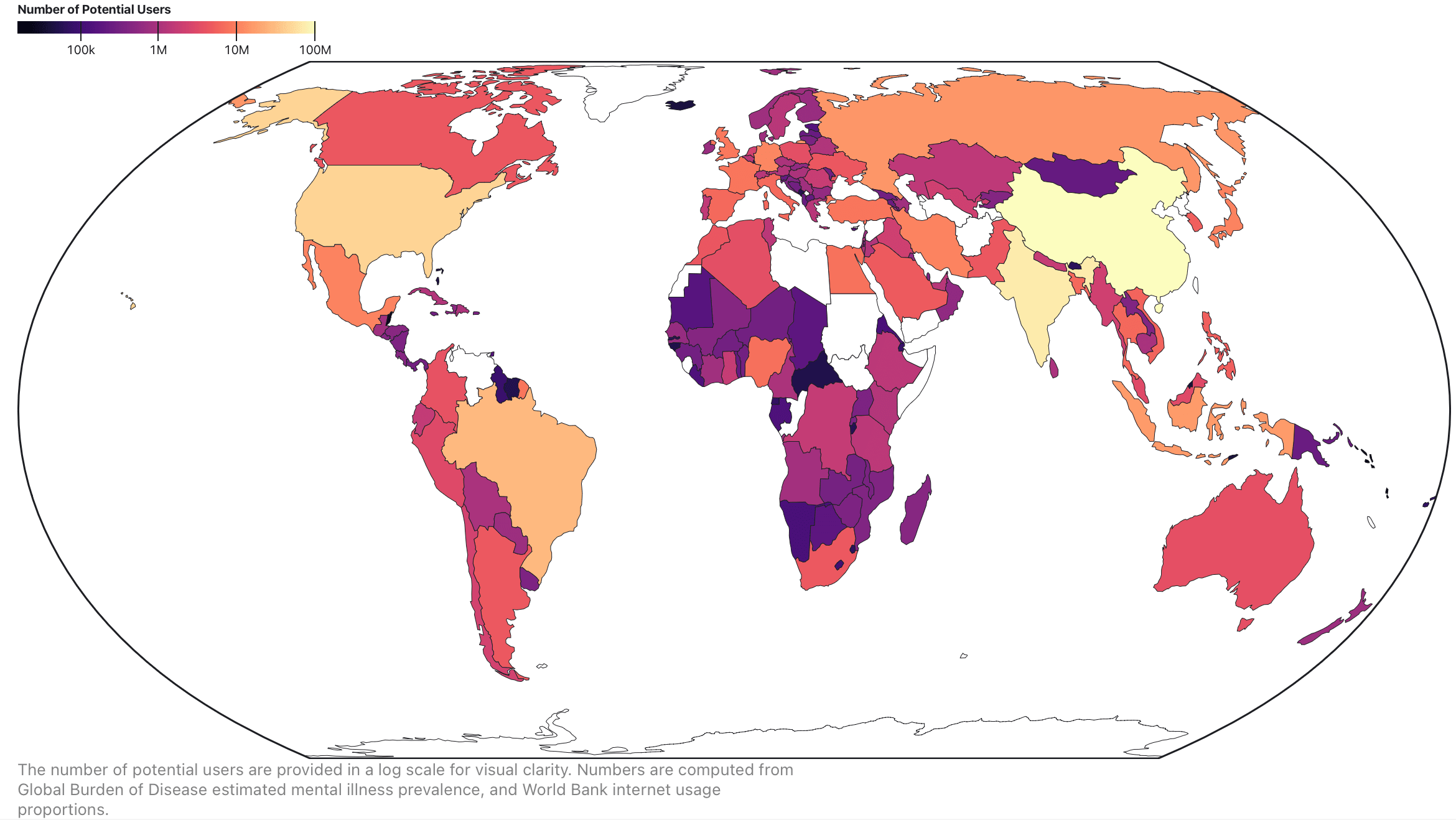

BetterHelp have served 8–10% of their addressable market, and currently serve 0.7–0.9%

Follow the working out in this Observable Notebook

Let’s assume that BetterHelp have still have that mid-teens international usage, which we’ll set at 13–17%. So with 407–476k total active users, they should have around 347–406k users in the U.S. Using the GBD, we can determine there are 47.1–54.7M U.S. adults with mental disorders. Furthermore, the World Bank estimate around 92% of Americans have internet access. Multiplying through, BetterHelp’s addressable market is then about 53.3–50.1M people.

Of this, they currently have 0.8% (0.7–0.9%) of that market actively subscribed to the service, and 8.8% (8.2–9.5%) of that market have ever tried the service.

BetterHelp claim that their top churn reason is affordability, which is likely having a strong depressive effect on their potential scale (it’s telling that, in response, they’re starting to pursue insurance coverage in the U.S.). As such, it’s hard to say what a more affordable product would look like. But, equally, it’s hard to imagine a much more affordable product without government subsidies (their usual margins are around 5–10%); from the consumer’s perspective, private health insurance is just a way of amortising costs, not a way of making therapy genuinely cheaper.

So I don’t think it’s unreasonable to treat BetterHelp’s U.S. market saturation as a genuine ceiling for a non-subsidised product. As such, we can extrapolate to other markets using the same formula—0.8% of mentally unwell, internet-connected adults should use it on an ongoing basis, and 8.8% of the same will use it at some point.

Here, then, are the appropriate ceilings (click through for an interactive chart):

| Country |

All-Time Potential Users |

Active Potential Users |

| China |

9,200,000 |

840,000 |

| India |

6,300,000 |

580,000 |

| United States |

4,100,000 |

370,000 |

| Brazil |

2,500,000 |

230,000 |

| Indonesia |

1,400,000 |

130,000 |

| Russia |

1,300,000 |

120,000 |

| Germany |

1,000,000 |

90,000 |

| Iran |

900,000 |

90,000 |

| Mexico |

900,000 |

90,000 |

| Japan |

900,000 |

80,000 |

| United Kingdom |

800,000 |

70,000 |

| Türkiye |

700,000 |

70,000 |

| France |

700,000 |

70,000 |

| Egypt |

700,000 |

60,000 |

| Nigeria |

700,000 |

60,000 |

| Spain |

600,000 |

50,000 |

Some of this isn’t too surprising; many of the top countries are the largest population hubs. However, larger countries such as Bangladesh, Pakistan, and Nigeria, rank unusually low due to lower depression rates & internet access, while countries such as Germany, Japan, and the UK rank higher than they ordinarily would. Furthermore, the U.S. is within the range of India and China, despite having a much lower population.

And that’s about it. I think this post is kind of boring, but I realised it was worth posting somewhere because I did a lot of data collection work that, to my knowledge, hadn’t been done before, and it was useful for me to ground my scale estimates for a couple of things.

I'm confused by this assertion. US employers commonly subsidize employee health insurance to the tune of ~70%. Most US employees [edit: do not have] a realistic choice between a job with employer-provided insurance and a much higher-paying job without it. For people eligible to receive Affordable Care Act subsidies, the subsidy can be up to nearly 100%. Medicaid is subsidized at essentially 100%, Medicare is subsidized at roughly 80%. So in a sense, the US government is subsidizing a lot of therapy . . . but only therapy provided as a benefit under government-run health insurance schemes, not through BetterHelp.

The actual cost of the insurance is irrelevant to the consumer, who will rationally consider only the portion of the cost that isn't picked up by the employer / the government.

On Medicare and Medicaid, I don't have any indication that BetterHelp are pursuing public insurance. If they were, I agree it would increase usage because the price would genuinely get cheaper for the consumer.

I am struggling to square these two statements. A rational consumer that is refusing a higher-paying job with no insurance is, in some sense, choosing to pay for that insurance. Or do people frequently choose lower-paying jobs with health insurance out of a sense of obligation, and then mentally treat the healthcare benefits as 'free'? (I really struggle to understand the US healthcare system because I don't interact with it).

Sorry! I left out a word by mistake: most US workers do not have a realistic choice between a higher-paying no-insurance job and a lower-paying insured job.

With that corrected, I'm still getting stuck on the "addressable market" and using BetterHelp's US market penetration to draw inferences about how big BetterHelp (or a comparable service) might fare in other countries. It seems to me that BetterHelp's market penetration is highly dependent on it being a cash-pay service in a country with an arguably unusual mix of competing insurance-subsidized products. Unfortunately, I think that limits the generalizability of your findings.

To take an extreme example, Medicaid is almost 100% subsidized for the consumer, and by definition Medicaid consumers are poor (otherwise they would not qualify). Because of these limitations, I'd model the universe of Medicaid consumers with mental illness as outside of BetterHelp's addressable market altogether under its current model, just like you've excluded non-Internet households. Then you have most other patient populations for which alternatives to BetterHelp are heavily subsidized by insurance, but not as that great an extent. It's hard to assess how many of those consumers are even plausible recruits for the current version of BetterHelp.

US consumers might have a number of reasons for using BetterHelp rather than an insurance-compatible option, such as:

I don't think BetterHelp's current US market penetration tells us much without considering how it stacks up against other options in the other country. For example, in a country like the UK, issues like lack of insurance, huge insurance deductibles/copays, highly restrictive provider networks, etc. shouldn't exist on the NHS. In other countries, subsidized options may not be available to most consumers or might not be decent substitutes for BetterHelp.

BetterHelp could start joining insurance networks in the US and thus start competing more effectively with insurance-subsidized traditional providers. However, its market penetration would become a much less reliable estimate of the potential size of the overall US teletherapy market than it is of the cash-pay market at present. I think it's likely that most insured patients would stick with solo / small-group therapists rather than migrate to a big platform.[1]

And I'm not convinced that joining insurance networks would be a good play for BetterHelp anyway. The insurance companies want discounts off your cash rate to list you in their network, and there's a significant amount of overhead involved in US insurance for the provider. So insurance-using patients are likely to be much less profitable. While you could think of these costs as a form of marketing spend, there's a deeper problem lurking here.

I suspect many current (or potential future) cash-pay patients have insurance but are choosing not to go through it for one of the reasons I listed above. For most of those use cases, a consumer would prefer BetterHelp + insurance over BetterHelp + cash-pay. For example, even if you have a $5K deductible and the insurance isn't going to actually pay for your therapy, you could still take advantage of the insurer's negotiated discount for BetterHelp by going through your insurance. So BetterHelp would have to figure out a way not to accidentally convert its cash-pay patients into much less profitable insurance-using patients.

I agree with most of this tbh, I am probably stretching with the generalisability of the findings. What I was roughly trying to get at was:

But I don't think I did a great job of communicating that as the through-line.