This is a linkpost for https://benjamintodd.substack.com/p/the-market-expects-ai-software-to

We can use Nvidia's stock price to estimate plausible market expectations for the size of the AI chip market, and we can use that to back-out expectations about AI software revenues and value creation.

Doing this helps to understand how much AI growth is expected by society, and how EA expectations compare. It's similar to an earlier post that uses interest rates in a similar way, except I'd argue using the prices of AI companies is more useful right now, since it's more targeted at the figures we most care about.

The exercise requires making some assumptions which I think are plausible (but not guaranteed to hold).

The full analysis is here, but here are some key points:

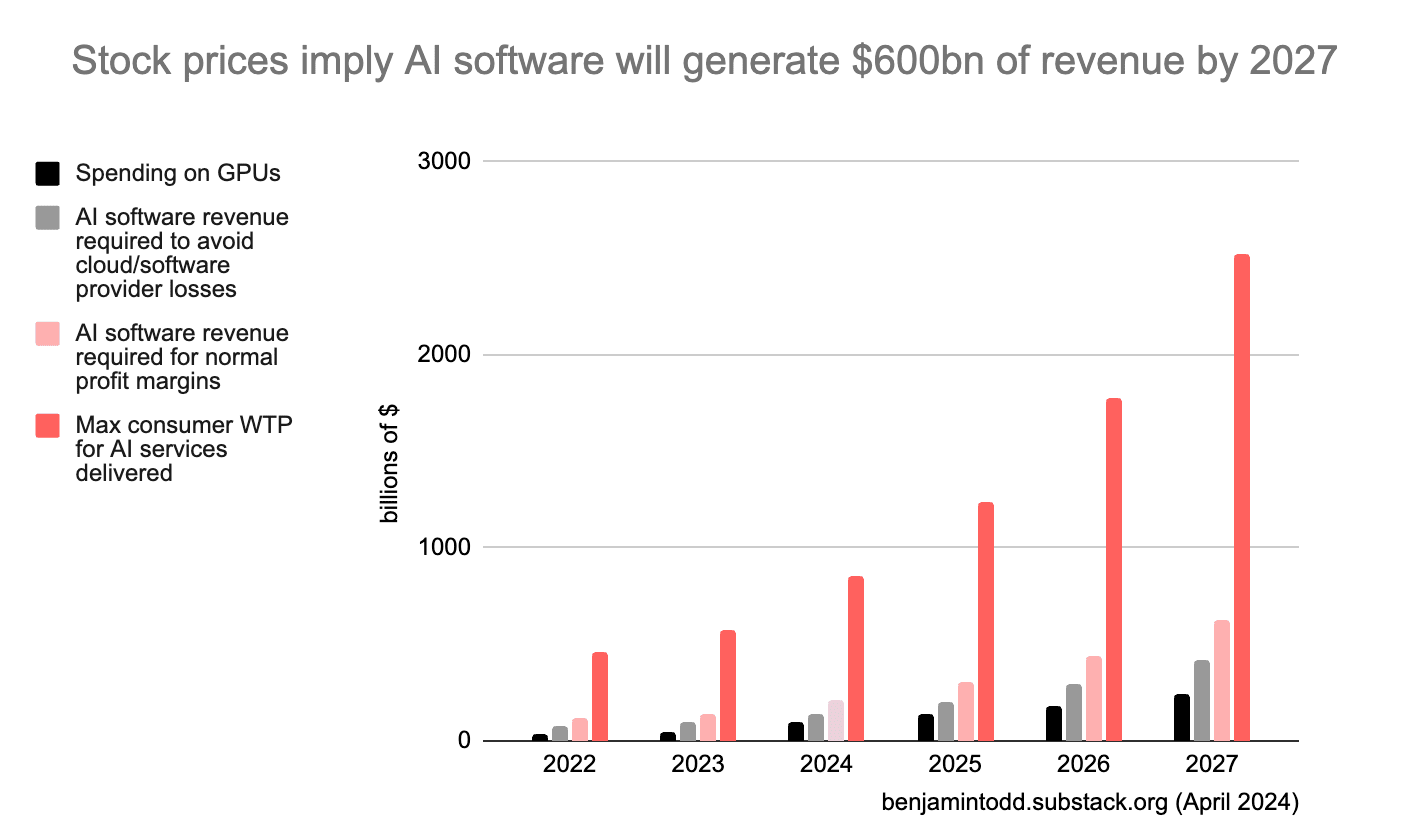

- Nvidia’s current market cap implies the future AI chip market reaches over ~$180bn/year (at current margins), then grows at average rates after that (so around $200bn by 2027). If margins or market share decline, revenues need to be even higher.

- For a data centre to actually use these chips in servers costs another ~80% for other hardware and electricity, then the AI software company that rents the chips will typically have at least another 40% in labour costs.

- This means with $200bn/year spent on AI chips, AI software revenues need reach $500bn/year for these groups to avoid losses, or $800bn/year to make normal profit margins. That would likely require consumers to be willing to pay up to several trillion for these services.

- The typical lifetime of a GPU implies that revenues would need to reach these levels before 2028. If you made a simple model with 35% annual growth in GPU spending, you can estimate year-by-year revenues, as shown in the chart below.

- This isn’t just about Nvidia – other estimates (e.g. the price of Microsoft) seem consistent with these figures.

- These revenues seem high in that they require a big scale up from today; but low if you think AI could start to automate a large fraction of jobs before 2030.

- If market expectations are correct, then by 2027 the amount of money generated by AI will make it easy to fund $10bn+ training runs.

I do think you should hedge more given the tower of assumptions underneath.

The title of the post is simultaneously very confident ("the market implies" and "but not more"), but also somewhat imprecise ("trillions" and "value"). It was not clear to me that the point you were trying to make was that the number was high.

Your use of "but not more" implies you were also trying to assert the point that it was not that high, but I agree with your point above that the market could be even bigger. If you believe it could be much bigger, that seems inconsistent with the title.

I also think "value" and "revenue" are not equivalent for 2 reasons: