This is a linkpost for https://benjamintodd.substack.com/p/the-market-expects-ai-software-to

We can use Nvidia's stock price to estimate plausible market expectations for the size of the AI chip market, and we can use that to back-out expectations about AI software revenues and value creation.

Doing this helps to understand how much AI growth is expected by society, and how EA expectations compare. It's similar to an earlier post that uses interest rates in a similar way, except I'd argue using the prices of AI companies is more useful right now, since it's more targeted at the figures we most care about.

The exercise requires making some assumptions which I think are plausible (but not guaranteed to hold).

The full analysis is here, but here are some key points:

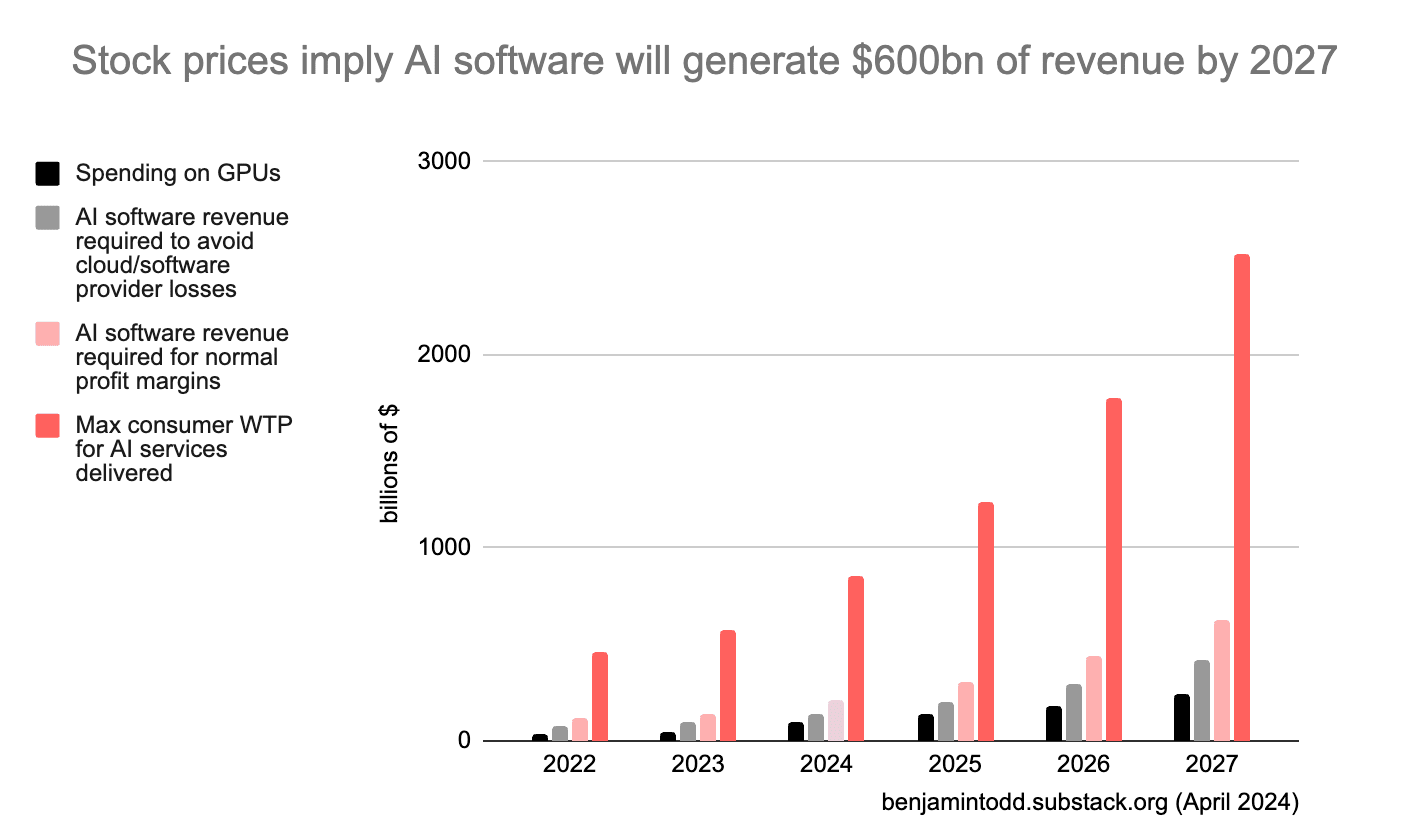

- Nvidia’s current market cap implies the future AI chip market reaches over ~$180bn/year (at current margins), then grows at average rates after that (so around $200bn by 2027). If margins or market share decline, revenues need to be even higher.

- For a data centre to actually use these chips in servers costs another ~80% for other hardware and electricity, then the AI software company that rents the chips will typically have at least another 40% in labour costs.

- This means with $200bn/year spent on AI chips, AI software revenues need reach $500bn/year for these groups to avoid losses, or $800bn/year to make normal profit margins. That would likely require consumers to be willing to pay up to several trillion for these services.

- The typical lifetime of a GPU implies that revenues would need to reach these levels before 2028. If you made a simple model with 35% annual growth in GPU spending, you can estimate year-by-year revenues, as shown in the chart below.

- This isn’t just about Nvidia – other estimates (e.g. the price of Microsoft) seem consistent with these figures.

- These revenues seem high in that they require a big scale up from today; but low if you think AI could start to automate a large fraction of jobs before 2030.

- If market expectations are correct, then by 2027 the amount of money generated by AI will make it easy to fund $10bn+ training runs.

Stock prices represent risk and information asymmetry, not just the P/E ratio.

The big 5 tech companies (google, amazon, microsoft, facebook, apple) primarily do data analysis and software (with apple as a partial exception). That puts each of the five (except apple to some extent, as their thread to hang on is iphone marketing) at the cutting edge of all the things that high-level data analysis is needed for, which is a very diverse game where each of the diverse elements add in a ton of risk (e.g. major hacks, data poisoning, military/geopolitical applications, lighting-quick historically unprecedented corporate espionage strategies, etc).

The big 5 are more like the wild west, everything that's happening is historically unprecedented and they could easily become the big 4, since a major event e.g. a big data leak could cause a staff exodus or a software exodus that allows the others to subsume most of their market share (imagine how LLMs affected Google's moat for search, except LLMs are just one example of historical unprecedence (that EA happens to focus way closer on, relative to other advancements, than wall street and DC), and most of the big 5 companies are vulnerable in ways as brutal and historically unprecedented as the emergence of LLMs).

Nvidia, on the other hand, is exclusively hardware and has a very strong moat (obviously semiconductor supply chains are a big deal here). This reduces risk premiums substantially, and I think it's reasonable likely that they would even be substantially lower risk per dollar than holding stock diversified between all 5 of the big 5 tech companies combined; I think the big 5 set a precedent that the companies making up the big leagues are each very high risk including in aggregate and Nvidia's unusual degree of stability, while also emerging on the bigleagues stage without diversifying or getting great access to secure data, might potentially shatter the high-risk bigtech company investment paradigm. I think this could cause people's p/e ratio for Nvidia to maybe be twice or even three times higher than it should, if they depend heavily on comparing Nvidia specifically to google, amazon, facebook, microsoft, and apple. This is also a qualitative risk that can also spiral into other effects e.g. a qualitatively different kind of bubble risk than what we've seen from the big 5 over the last ~15 years of the post-2008 paradigm where data analysis is important and respected.

tl;dr Nvidia's stable hardware base might make comparisons to the 5 similarly-sized tech companies unhelpful, as those companies probably have risk premiums that are much higher and more difficult to calculate for investors.

My bad- I should have looked into Nvidia more before commenting.

Your model looked like something that people were supposed to try to poke holes in, and I realized midway through my comment that it was actually a minor nitpick + some interesting dynamics rather than a significant flaw (e.g. even if true it only puts a small dent in the OOM focus).