Comments

Thanks for sharing, Lizka! and thanks to everyone else for sharing their voices in the comments too!

I liked this post from Samie which talks about some factors for financial planning and security that are helping when thinking about donating - I liked the ideas about income protection insurance and thinking about financial goals.

I personally took a trial pledge for 3% of my income for a year before deciding I could really commit to the full GWWC Pledge. I've had ongoing health issues throughout my adulthood which at times meant I wasn't able to work full time and was concerned about my ability to potentially earn an income in the future - so it was a really big deal to me to sign a lifetime pledge.

There were a couple of things that pushed me over the edge to take the full pledge:

- Feeling like I did have enough saved that if I had to reduce my work hours that I could still afford to donate. I've been fortunate to be working from the age of 20 and lived with my parents for many years so I could save money.

- Knowing if that if I couldn't work anymore that I wouldn't be liable for donations under the pledge (just a suggested 1% of spending money) or that I could always resign if I needed to. On this point, I didn't want to let the fear of my health potentially declining be a reason not to make an important commitment to do good - I like the marriage analogy with the pledge, as mentioned by others here.

- Knowing that even on a modest income in Australia (or even on government benefits), I would still be really well off in comparison to the majority of people alive right now. My own health issues and suffering have been a big part of understanding how positively my donations could impact the lives of others, and I find that really personally motivating.

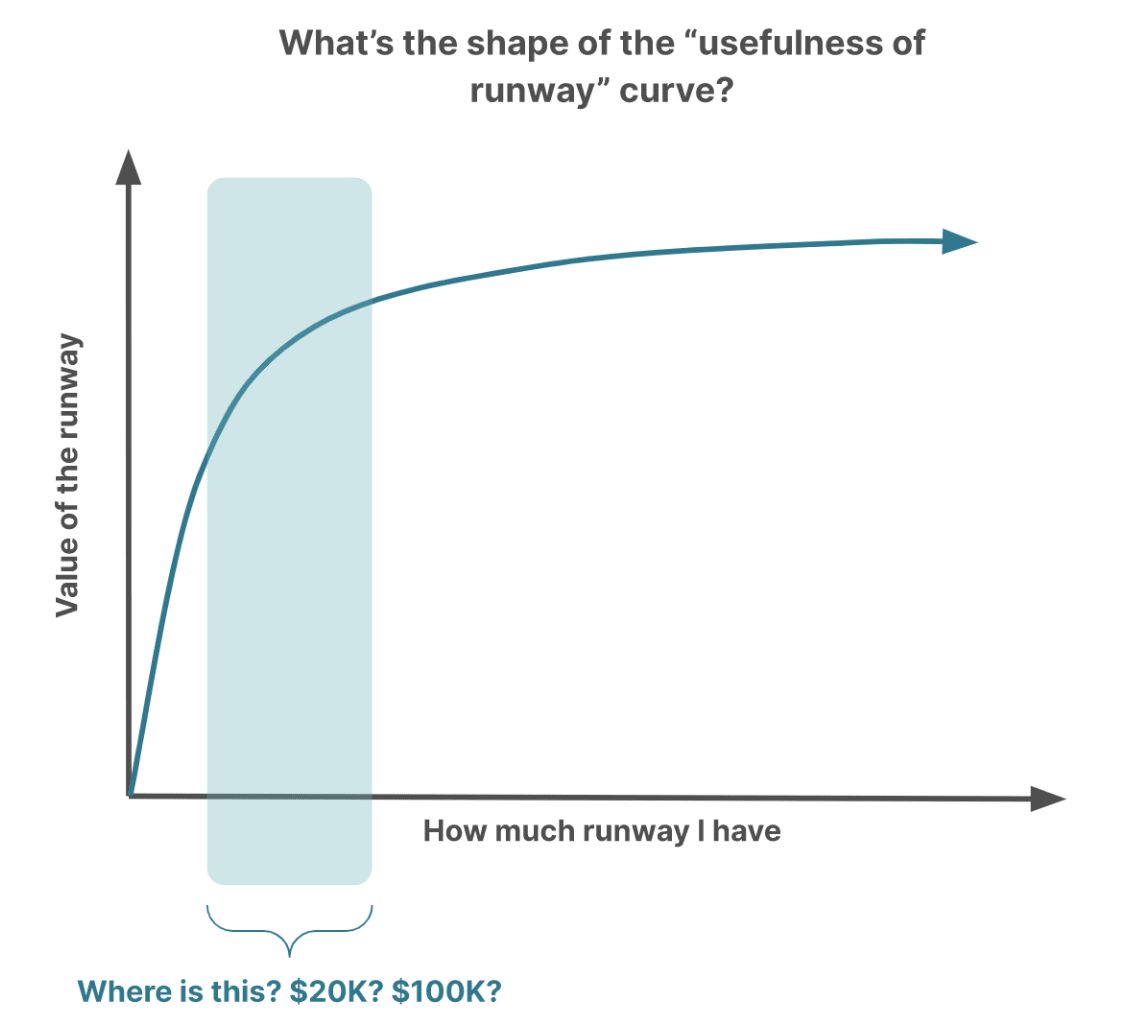

I think it's really up to each individual to figure out how much runway to save up, because our circumstances are all quite different (i.e. family, health, government policies, likelihood of changes to income level etc). I do think it was easier for me to sign a lifetime pledge because I have a family who are likely to be able to support me if things were really dire.

Taking the GWWC Pledge is a big commitment and I would recommend that people think carefully about it before doing so. I think a Trial Pledge is a great step and I'm really excited about the value of having people show that they're donating on a public register, even without the lifetime commitment, because this helps normalise effective giving and giving more broadly as a positive social norm!

(I work for GWWC but this was written in my personal capacity)

Thanks for sharing this! It's great to have some honest and open conversations about the GWWC pledge.

FWIW I think perceived wisdom is that around 6-12 months of living expenses is pretty good as an emergency fund, which might help in terms of your runway value curve. For example, that might look like £1.8k per month (which I think is roughly the UK average) x 6-12 = £10-20k. Ideally, this would be in instant access savings, rather than stocks (but this isn't true in my case).

Other thoughts: I think unless you expect your situation to change dramatically in the next year (e.g. you leave your job), it seems reasonable that you could both save for an emergency fund (at least partially) and donate 10%? For example, if you have a salary of £50k, that's a takehome salary of £37k, which might be broken down like:

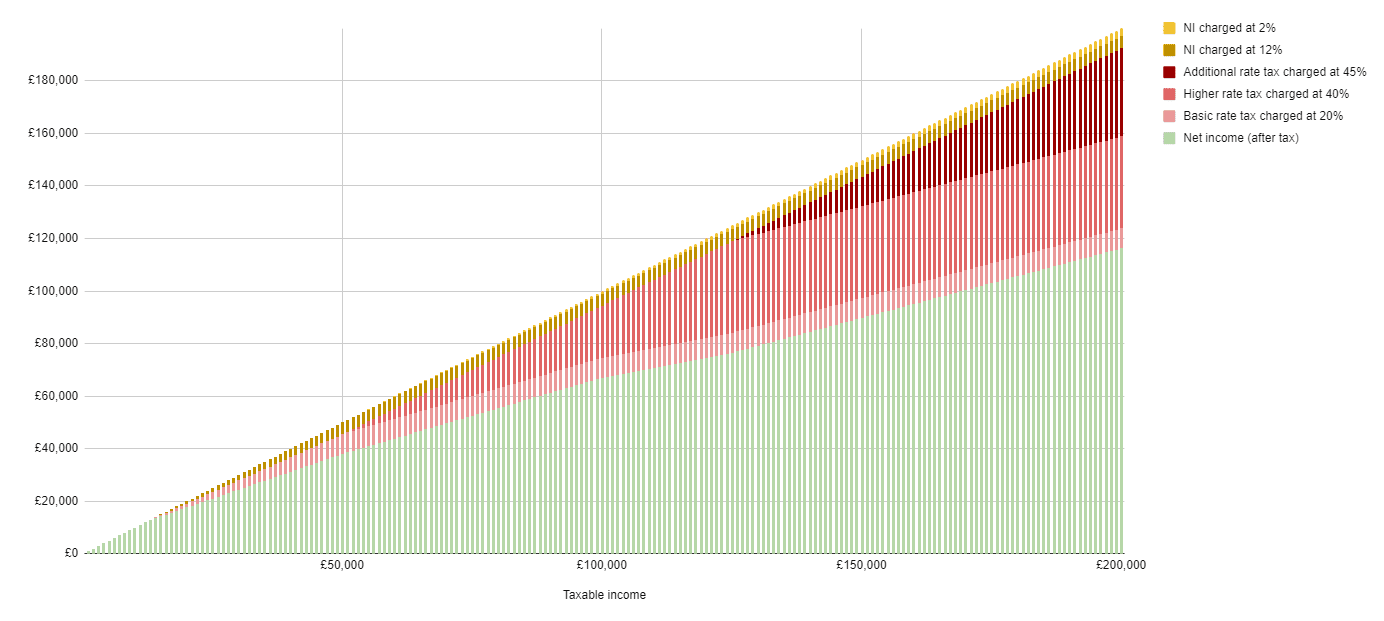

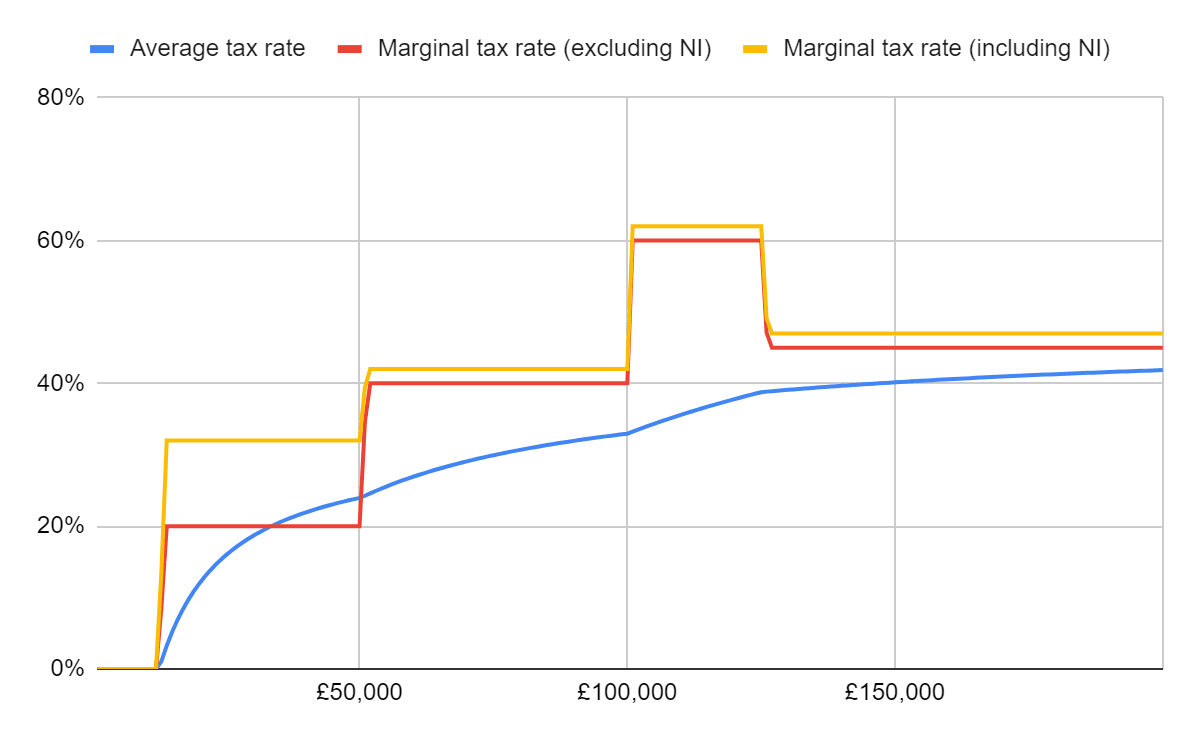

Great comment - I'd add that usually GWWC pledges in the UK are based on pre tax so it wouldn't actually cost the full £5k. Donations reduce your income for income tax purposes (but not NI) - Payroll Giving (UK) or GAYE - EA Forum (effectivealtruism.org)

ie.

£50k salary

£3.75k donation which is grossed up by 25% from your taxes with gift aid to £5k

If you actually donated £5k then that would be a £7.5k total donation when grossed up with gift aid.

However, the higher rate tax (40%) band starts at ~£50k a year so every £1 donated above that costs 60p

(Working on a longer explainer on this which updates this piece UK Income Tax & Donations — EA Forum (effectivealtruism.org) but you can check out the underlying spreadsheet which create these graphs here: UK Income tax (including NI) - Google Sheets)

I love this breakdown, and it emphasises an important point (that was not mentioned in the post) that living expenses might actually be the highest variation, and often most critical factor in determining how much we might be capable of both giving and saving.

Oh yeah, a big one.

It was a combination of reading about Toby and the further pledge at the same time as reading some behavioural economics and learning about the hedonic treadmill that led me to switch our finances to "pay ourselves a living allowance" at a time when we were on a very low combined income and as our incomes grew so did both our savings and donations. It was because of the lower spend rate more than the savings that I felt able to take the risk of pursuing startups, big pay cuts to work in nonprofit sector, and we both took time off between jobs in 2019. It's certainly a privilege that not everyone has (e.g. things like living in a country with reasonable basic public healthcare certainly helps), but it's something that I've seen many peers not pursue (no matter how much they earn, just always spend what's in their account) and then look upon me enviably when I'm pursuing things that give me more meaning.