Executive Summary

- EAs can use capital markets to grow their wealth, in order to donate more later in life or free up time to do impactful things.

- Evidence suggests that investing that money into sustainable investments provides marginal positive impact, stronger returns, and is unlikely to pose additional risks.

- Most people don’t invest (including EAs) because they lack guidance. We have built SageWealth in order to make investing more accessible.

- The long-view of SageWealth is to become the sustainable investment bank (think UBS) for Millennials and Gen Z.

- The founders consider this a ‘founding to give’ project and hope to have a meaningful influence on the conversation on sustainable investing and nudge it towards EA values.

1. What is 'investing to give'?

In a nutshell, ‘investing to give’ means that you make use of capital markets to grow your wealth (or at least protect it from shrinking). One can then use this additional wealth to do more good. This can be an especially interesting strategy if an EA is waiting for an outsized giving opportunity to donate to.

At a minimum, you can secure your retirement. Even better, you could free up your own time for working on impactful projects, and even better, you could donate (as much as) 1,568% more later in life [1].

1.1 The dangers of not investing

For those of you keeping your wealth in Euros, that wealth has lost 11.5% of its value in 2022 alone, due to inflation. Although most years are not so punishing, generally speaking, it’s not a good idea to keep too much in cash. Over the past 30 years, the inflation rate in Europe has been about 2% per year. While that might not sound like much, it means you lose ~50% of your wealth over a 40-year period. This means less money to donate, retire well, work on pressing problems independently or save enough money so you can donate your time.

1.2 The market grows faster than you think

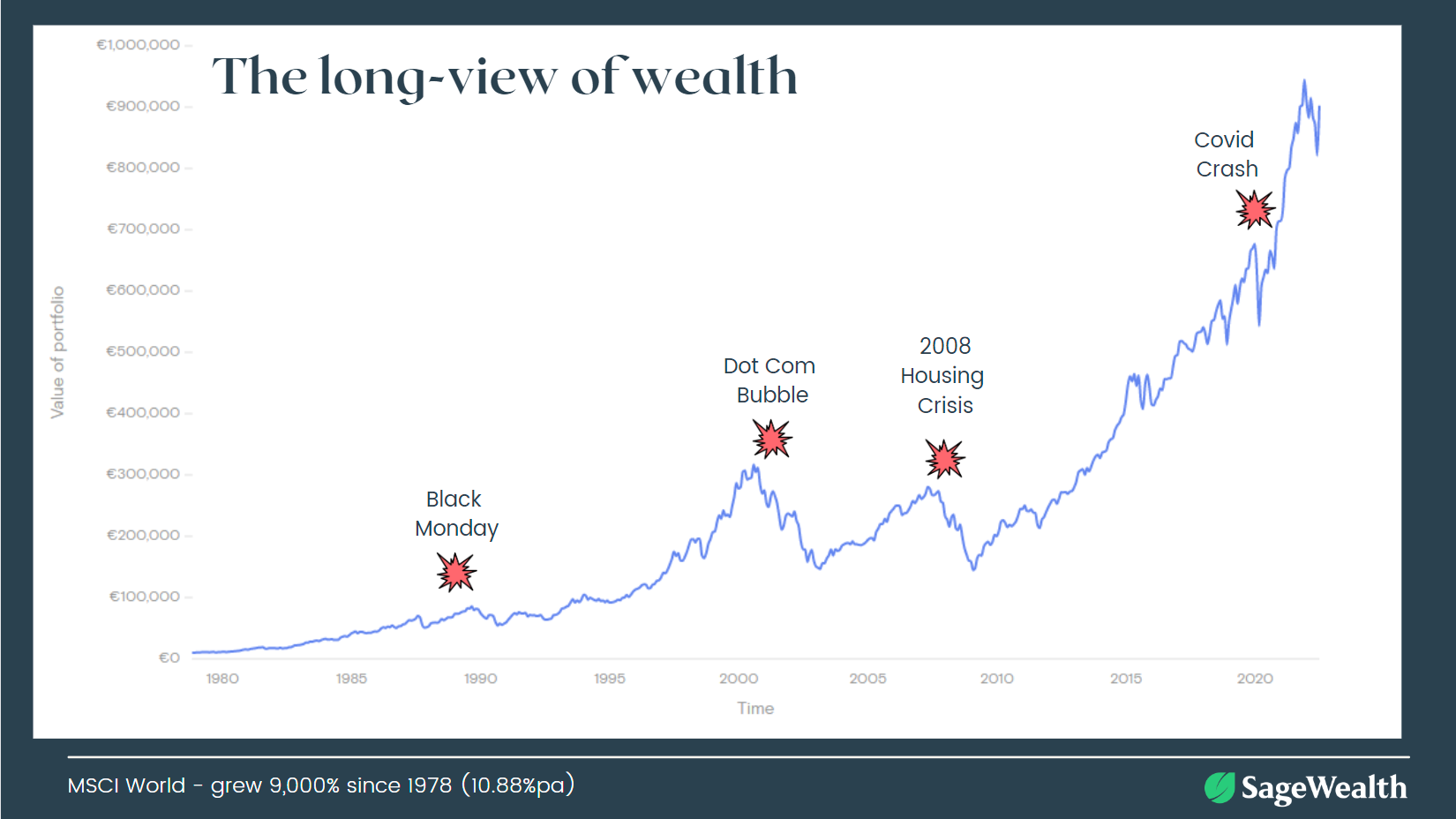

A globally diversified investment product, like 'MSCI World' has grown on average by 10.94% per year since 1978. Similarly, the S&P 500 (which has been around since 1928) has grown by 11.82% on average per year since inception. Nobody knows for sure whether these same rates of growth will continue into the future. But if you are of the belief that human ingenuity and problem-solving will continue over the coming decades, then it’s not crazy to extrapolate this kind of growth forward. Please note, however, that historic returns cannot predict future returns, and should only be seen as a reasonable indicator.

Now, this is not to say that investing comes without dangers. As you can see in the graph above, markets are volatile. This means that in the short-term, markets can drop, and if you sell your investments during these periods, you will lose money.

However, so long as you are investing passively over longer periods of time, then markets will mostly work in your favour. The yield triangle for MSCI World shows your chances of making a profit over the past 40 years: If you keep your money invested for 5 years, you have a 77% chance of making a profit; after 10 years this goes up to 90%; and after 15 years this goes up to 100%. You can do similar calculations for the 90 years of the S&P 500 (which went through two World Wars) and the results are quite similar. Again, long-term historical averages cannot predict future returns, and these probabilities are only intended to give you reasonable estimates.

1.3 What does this mean for you?

In his Twitter thread, Robert Wiblin argues that helping someone set up a good retirement system is very impactful because they could be hundreds of thousands richer later in life.

A similar point is made by Tobias Leenaert (author of ‘How to Create a Vegan World’). He notes that most vegans and those working in animal rights charities don’t invest, and have moral qualms with having wealth. In his own words, 'I also believe that more money in the hands of good, caring people is a good thing and that the do-goodies shouldn’t leave the making of money to the greedy ones.'

We like to think of investing as a tool, one that if used properly (over long periods of time) can grow your money (so long as you can stomach the short-term volatility). Here are several ways in which you can use investing for good:

Protect your wealth from inflation: Rather than losing -2% of your wealth per year, you can grow it instead.

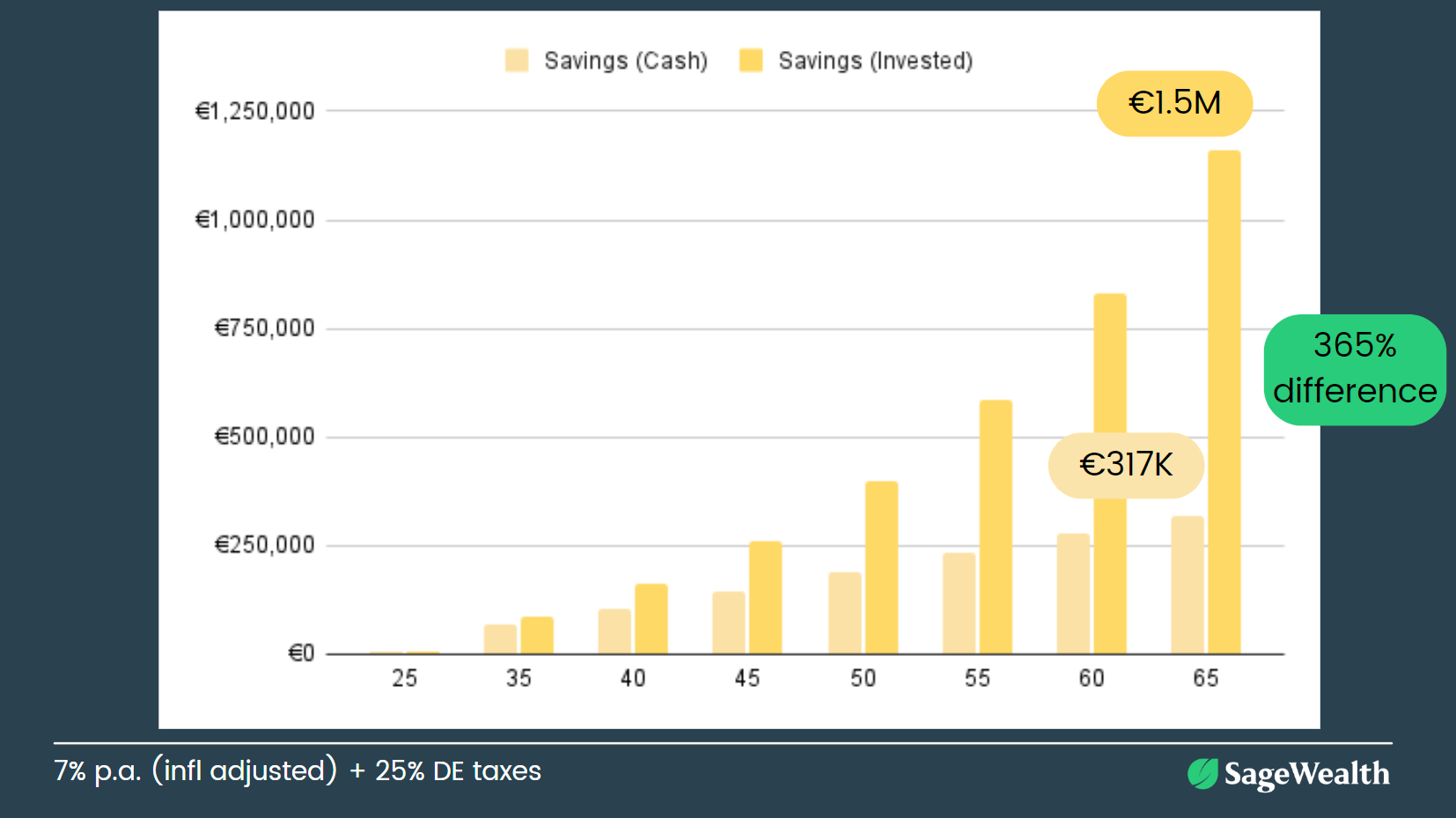

Secure your retirement: You can retire 365% wealthier if you invest, than if you don’t invest (based on historic market growth). This calculation is done by analysing the change in lifetime income of Germans with a university degree. If this average German saved 20% of their salary each year[2] (starting at the age of 20), they would be able to save up to €317,000 by the time they are 65. However, if this same person invested that money in the stock market during that period, they would retire with €1.2m[3]. This is a +365% difference in wealth at retirement!

Retire early or work part-time: Having additional wealth throughout your life could mean you can retire at an earlier age and work on impactful projects. For example, you could use something akin to the 4% rule to live off passive income from your investments. Note that ‘rule’ is only a rule of thumb, and you will need to do a bit more planning to make sure you have a comfortable retirement.

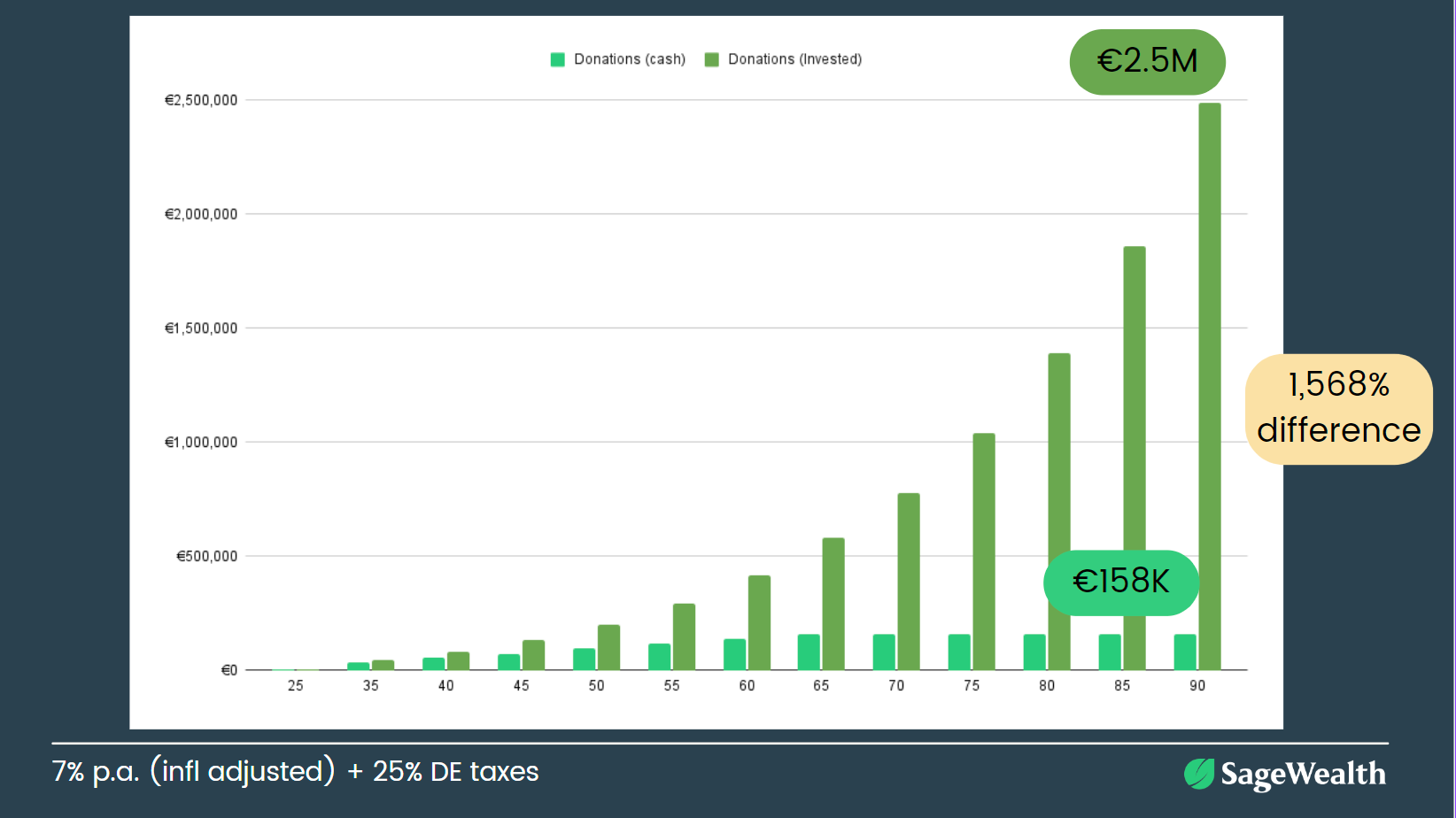

Donate more later in life: If that same average German with a university degree donated 10% of their income each year, they would be able to donate €158K throughout their life. Alternatively, if they invested this money and donate it all upon death, they could donate €2.5m (1,568% more[4]). Of course, there are also many options in between. For example, one could donate 5% of income each year and invest another 5%.

Mind you, we are not making a case for donating now vs donating later. Rather, we want to showcase that there are tools available in case you are inclined to donate later.

2. Where you invest matters (a bit)

In the past decade, there has been an explosion of (so-called) 'sustainable investments' or 'impact investments' on the market. Are they impactful? Kind of. Are they worth investing in? Absolutely!

2.1 What is sustainable investing?

Sustainable investing tends to mean that you chose to invest in some set of companies over others due to ethical criteria. This is great in principle, as it allows one to support companies that better align with one's values. But in practice, it has many limitations.

One common method used is called ESG which stands for Environmental, Social and Governance issues (more about this here); Another is Social Responsible Investing (SRI). Although SRI usually has stricter ethical standards than ESG, but the key problem is that neither has any standard methodology for how they work.

Sanjay Joshi and Ellen Quigley wrote a great piece on this called ‘ESG investing is wholly misdirected’. Among many problems, they point out how ESG frameworks will often compare companies with each other (rather than use an independent metric), which can result in giving harmful companies a good score, simply because they are slightly better than a competitor. This might mean that a tobacco company can still be considered ESG because it treats its employees well and has waste-efficient factories.

Socially Responsible Investing (SRI), on the other hand, usually has stricter ethical criteria and often tries to cut out entire industries because they are deemed harmful. For example, SRI funds will commonly exclude tobacco companies as a whole, because tobacco is always harmful to people. But again, this isn’t always the case. There are plenty of ‘greenwashed’ SRI investments that will include harmful companies (e.g. ExxonMobil instead of nuclear energy).

In summary: The good news is that there are good sustainable investment options out there. These will often protect you from investing in industries that are causing harm (weapons, tobacco, fossil fuels), and will also ensure you are investing in companies doing more good (renewable energy, vegan companies, etc). The bad news, however, is that it’s very difficult for a layperson to tell them apart without digging deep into the data.

2.2 Is sustainable investing impactful?

First off, we agree with many members of the Effective Altruist community, and specifically with Hauke Hillebrandt and John Halstead conclusions in their Impact Investing Report (2018) that donating is more impactful than socially responsible investing and/or impact investing.

However, there will always be money that cannot be donated, such as money one needs for retirement. Therefore, we would rephrase the question as follows:

For the money that you won’t donate, is it impactful to invest your money sustainably (when compared to keeping that money in cash or investing it non-sustainably)?

There are previous Effective Altruism forum posts showing that most forms of sustainable investing most likely have little impact. But there’s hope! In 'Is impact investing impactful'? John Halstead argues the following:

Contra EA conventional wisdom, SRI could be worthwhile! Investors should expect to have at most a modest direct effect on stock prices, on the margin. However, the existing noisy evidence suggests that SRI may not involve financial sacrifice, so could well be worth doing vs socially neutral investing.

In summary: At worst, SRI has a modest positive impact, and bears no additional sacrifice to the investor (see next section).

2.3 Sustainable investing is probably good for your returns

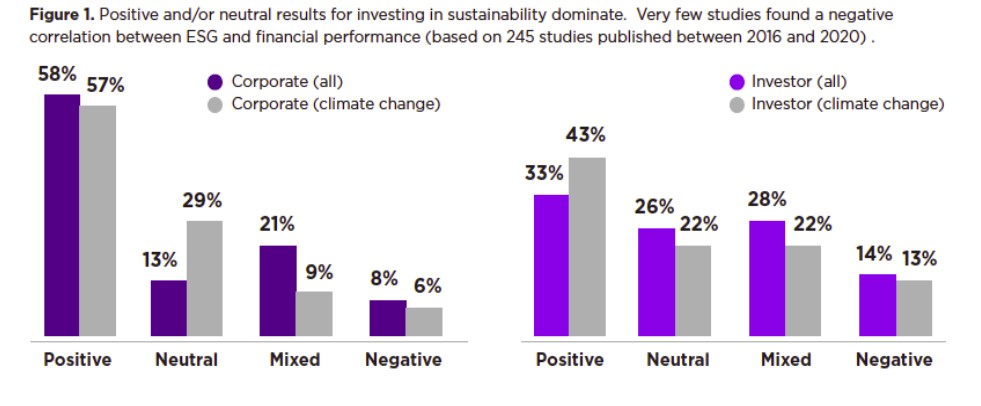

The two most widely cited meta-studies on the topic show that ESG investing (including SRI) outperforms traditional investing. An NYU Stern study (2021) shows that 57-58% of the time ESG investing yielded financial outperformance. And Friede et al (2015) show that ESG investing created better returns 48-63% of the time.

From this perspective, there isn’t really a good argument against ESG (and especially SRI investing). Even if the impact is marginal, it’s still the wiser investment decision when it comes to risk and returns.

2.4 Will this outperformance continue into the future?

While it is perfectly possible that the outperformance we see to date is nothing more than a trend that will die down, there are fundamental and underlying reasons to believe that the outperformance of sustainable investing may continue. The following section is very speculative.

One common argument for why outperformance exists is that ESG / SRI acts as a quality control on the company. It selects for companies that are well-managed, think long-term or are taking precautionary measures against risks.

According to McKinsey, ‘ESG issues can have a measurable effect on a company’s market value, as well as its reputation. Companies have seen their revenues and profits decline, for instance, after worker safety incidents, waste or pollution spills, weather-related supply-chain disruptions, and other ESG-related incidents have come to light. ESG issues have harmed some brands, which can account for much of a company’s market value.’

This is because ESG is often about improving a company’s risk management. Evidence shows that companies that take into account ESG also have lower volatility, which is a financial measure of risk.

Another argument is to focus on the fact that ESG companies are more involved in the pressing issues of our time, and as such are more likely to be in growth industries or working with cutting-edge technology. In Bill Gates' words,

Getting to [carbon] zero will be the hardest thing humans have ever done,' Gates writes in his year-end letter published Tuesday. 'We need to revolutionise the entire physical economy—how we make things, move around, produce electricity, grow food, and stay warm and cool—in less than three decades.

As such, Bill Gates believes climate tech will produce 8 to 10 Teslas, a Google, an Amazon and a Microsoft. Similarly, Larry Fink (CEO of Blackrock) stated

The next 1,000 unicorns won't be search engines or social media companies, they'll be sustainable, scalable innovators – startups that help the world decarbonize and make the energy transition affordable for all consumers

However, in order for a company to benefit from ESG, it has to be correctly implemented (mind you, many companies do not). According to Harvard Business Review, companies have to clearly establish which ESG issues they’re most financially and operationally affected by[5].

For example, life insurance companies are very affected by the health of their customers. These directly influence their bottom lines. Customers with good health have both a positive societal impact and cost the insurance company less money.

A notable forerunner here is the global life and health insurance company Discovery. They successfully tied their own financial incentives to that of the positive outcomes of their customers. For instance, they distributed free smartwatches for tracking health and exercise goals to their customers and implemented a sophisticated set of rewards based on living a healthy lifestyle. From the HRB article:

Rigorous academic studies by RAND, Johns Hopkins, and others have shown that the medical costs of Discovery’s health insurance subscribers are 15% lower compared with those insured by local competitors, and the life expectancy of Discovery’s life insurance customers is 10 years longer.

For these reasons, we think companies that score highly on ESG metrics have a very plausible chance of continued success.

2.5 Your bank probably sucks

Another angle to consider is the counterfactual of where you would keep your money.

Unfortunately, there is strong evidence that your bank is probably doing a lot of harm by loaning your money to harmful industries (e.g. fossil fuels). This is because it has become very hard for fossil fuel companies to raise money through equity.

Ellen Quigley argues that it can be impactful to remove money from banks or switch banks. 'If you look at new money that's flowing into fossil fuels, about 90% of it comes from debt. (...), you end up with a picture in which banks are your primary target: they're the ones controlling or directly contributing this money to these new uses'.

And this is consistent with the ‘Banking on Climate Chaos’ report, which is a joint effort between Rainforest Action Network (RAN), BankTrack, Indigenous Environmental Network (IEN), Oil Change International (OCI), Reclaim Finance, and the Sierra Club. They report that banks are the biggest funders of fossil fuel companies:

'Fossil fuel financing from the world’s 60 largest banks has reached USD $4.6 trillion in the six years since the adoption of the Paris Agreement, with $742 billion in fossil fuel financing in 2021 alone.'

Currently, the great majority of Germans (and Europeans) keep most of their savings in cash, and most of that sits with unethical banks. So by getting people to invest a significant amount of their savings sustainably, you are essentially divesting money away from fossil fuels.

2.6 There aren’t enough EAs influencing sustainable finance

Sanjay Joshi previously wrote on the EA forum that EA is missing out on a 100 trillion dollar opportunity. He argued that ESG is tractable, neglected, and scalable and trillions are likely to change their investment strategy based on how 'sustainable investing' is defined today. Therefore, we believe that investing with EA-aligned sustainable investment companies can put EAs in a better position to influence the way ESG is defined and implemented over the coming decades.

3. Introducing SageWealth

3.1 Who is behind SageWealth?

SageWealth is a sustainable digital wealth management platform. We help our clients better understand their current financial situation and set financial goals (eg. buy a home, retire early, or donate €200K to high-impact charities). We then provide sustainable financial products (such as ETF portfolios) to meet their goals faster.

SageWealth was founded by Marco Vega and Sana Al-Badri (hi!).

Marco is an avid futurist, who co-wrote 'An Introduction to Transhumanism', and was previously the founder of Nootropics.com. Marco previously interned at the Effective Altruism Foundation (Switzerland) and was personally mentored by suffering-focused ethicist and Transhumanist, David Pearce.

Sana ran an EA student group at Sussex University (UK), has worked as a UX-lead at a venture-funded startup (Mitte), and is a licensed financial advisor. Sana also worked on editing the 10th year anniversary edition of 'We Love Dogs, Eat Pigs, and Wear Cows' by Dr Melanie Joy, with a new foreword by Yuval Harari.

Both founders worked together at ProVeg International (a 'stand-out charity' according to ACE at the time), and they donate 4% of their annual income to high-impact charities (such as Give Directly, Clean Air Task Force, Animal Welfare Fund, and others).

We incorporated as Sagefund Digital Wealth Management GmbH in Berlin in early 2020 and secured partnerships with two renowned German banks (Bank für Vermögen and Baader Bank). Since launching in mid-2021, we are now managing €1.4M in our clients’ assets. Due to our rapid growth, we have raised a €500,000 pre-seed investment from top European business angels, such as the founders of Clue, Nebenan.de, and Crosslend.

3.2 Why SageWealth?

Millennials will inherit €65 Trillion by 2030, but nearly 80% of them currently don’t invest and don't possess basic financial literacy skills. 59% need financial advice and are willing to pay for it.

And from our experience so far: Most Effective Altruists don’t invest either!

Novice investors need a lot of educational content, tools & personal touch to build up the knowledge and trust necessary to start investing. In our personal experience, this process takes months for most people. Note, that we advised friends and family long before starting SageWealth and we observed this pattern.

For Americans: Think of us as the sustainable version of Wealthfront or Betterment, but in Europe.

Our long-term vision is to become the digital and sustainable UBS for Millennials. We want to help more people benefit from the growth of capitalism, and we want to have an EA influence on the sustainable investing conversation, which could influence trillions of Euros in the coming decades.

3.3 Our products and services

Financial advisory

We offer free 25 min financial planning calls via Zoom which can be booked via our website. Here we explore their financial situation, help them set goals, and recommend an investment strategy for them to best reach their goals. If the person is new to investing, we are happy to explain the basics investing.

Investment portfolios

We offer two investment portfolios that can be set up via our online onboarding process:

- SageWealth Stability: Designed for short-term goals (3-7 years). It’s composed of 70% bond ETFs and 30% stock ETFs and has a medium volatility (SRRI risk class: 4 of 7).

- SageWealth Growth: Designed for long-term goals (7+ years). It’s composed of 100% stock ETFs and has high volatility (SRRI risk class: 6 of 7).

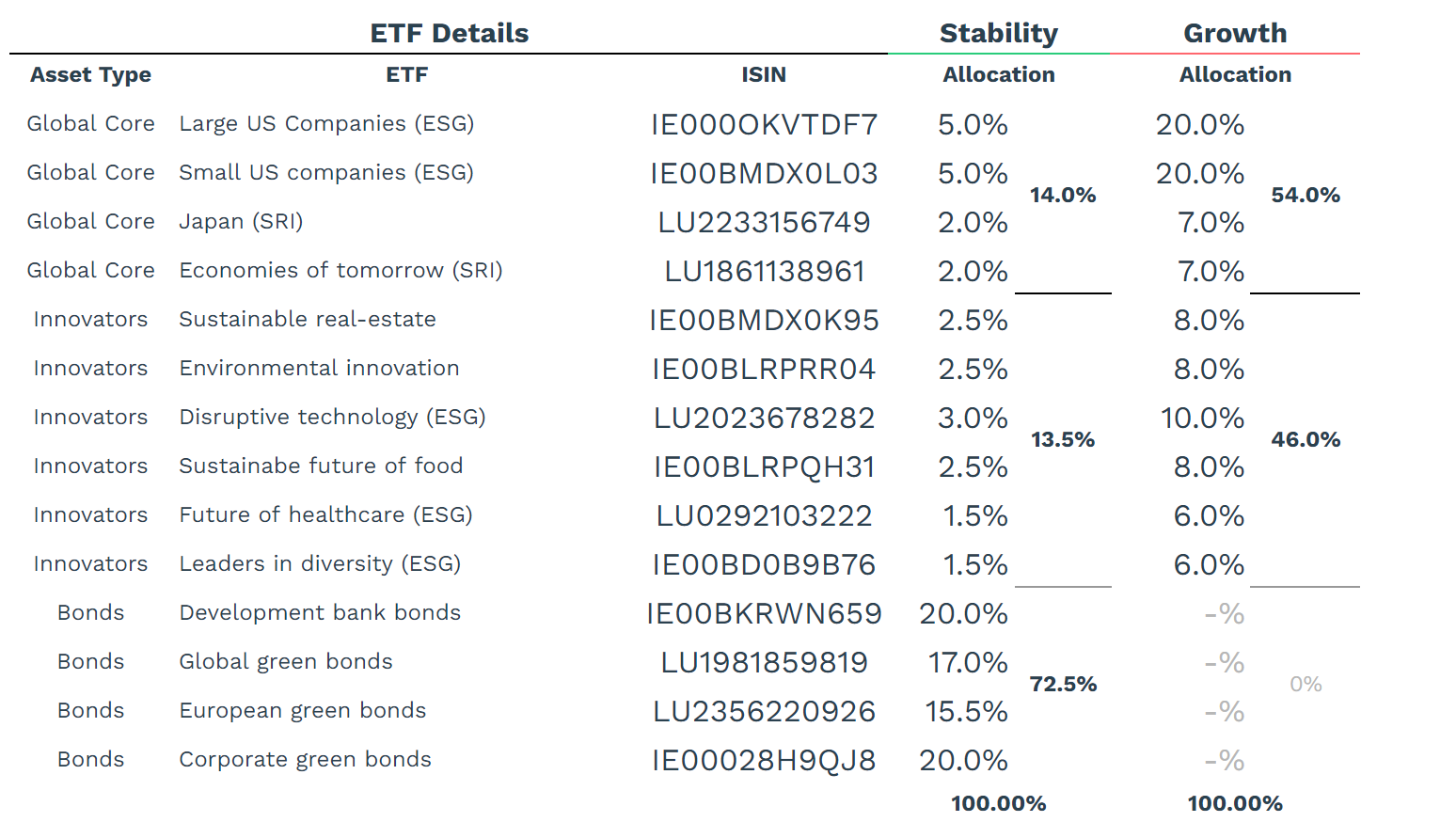

The ETFs inside the portfolios

The strategy behind the portfolios

- Have the highest possible rate of creating wealth

- Have the lowest possible risk while attempting to create wealth

- Cause the least harm possible

- If it doesn't compromise rule 1-3, then have a positive impact

We use Modern Portfolio Theory (MPT) to construct our portfolios. MPT is‘a practical method for selecting investments in order to maximise their overall returns within an acceptable level of risk’.

The 'Global Core' parts of the portfolios are made of broad market indexes. This ensures that your wealth is diversified globally into different geographic markets. Included are large and small US companies, Japan (which represents much of the Asian market), and Emerging Markets (which includes China, India, Brazil and others).

The 'Innovator' portion is made up of 'Thematic ETFs', these are ETFs which focus on specific industries and trends (rather than geographies). Thematic investing allows us to have more control over the companies inside the portfolio (and hence increase the sustainability rating). For example, the Sustainble Future of Food ETF is made of global companies that ‘stand to benefit from the accelerating transition to more sustainable food production systems and consumption patterns’, e.g. companies involved in plant-based food, precision farming and water technology.

With the 'Innovators', we are able to tilt our portfolio towards trends that have a high likelihood of being relevant over the next 20-30 years. This does mean our portfolios have a larger percentage of small-cap companies in our overall portfolios, which is likely to both increase returns and volatility.

The 'Bond' portion is made up of both development bonds and green bonds. These are effectively loans provided to developing countries to further develop their infrastructure, or bonds with the express intent of reducing climate emissions, such as electrifying their national train lines.

The portfolios were constructed by in collaboration with the founders of Sustainable Market Strategies (SMS) and Nordis Capital. They are also the research team behind popular RIZE ETFs, such as the Sustainable Future of Food ETF and Environmental Impact 100 ETF. SMS is also an investor in SageWealth.

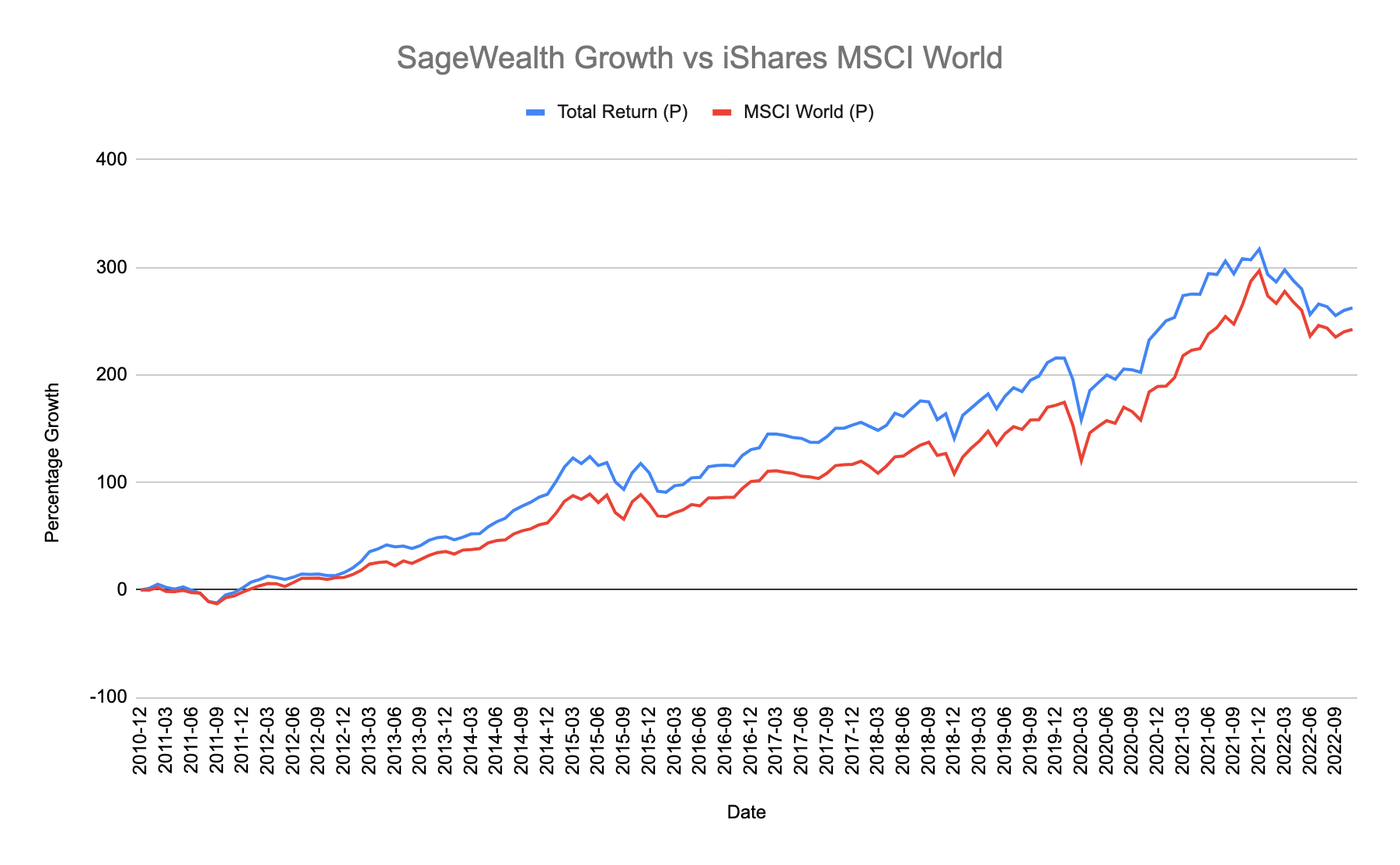

Below you can also see a performance comparison between SageWealth Growth[6] and MSCI World, a popular global ETF (between Jan 2011 until Dec 2022). For most of this period, SageWealth Growth outperformed MSCI World, and as of Dec 20 2022, it was ahead by +4.24%.

Pros and Cons of SageWealth

| Advantages | Disadvantages |

|

|

3.4 How SageWealth makes money

On a monthly basis, we charge a percentage of your total investment size. You can calculate the fees on our website.

- Accounts under 100,000 EUR pay 0.99% per year

- Accounts larger than 100,000 EUR pay 0.69% per year

The costs above include the fees for the ETFs[8], the transaction/banking/compliance fees, and our own fees.

Here’s the detailed breakdown:

- Baader Bank: 0.20%

- Bank für Vermögen: 0.06%

- ETF costs: 0.23% (Stability) or 0.28% (Growth)

- SageWealth: 0.15% (accounts above €100K) or 0.45% (accounts under €100K)

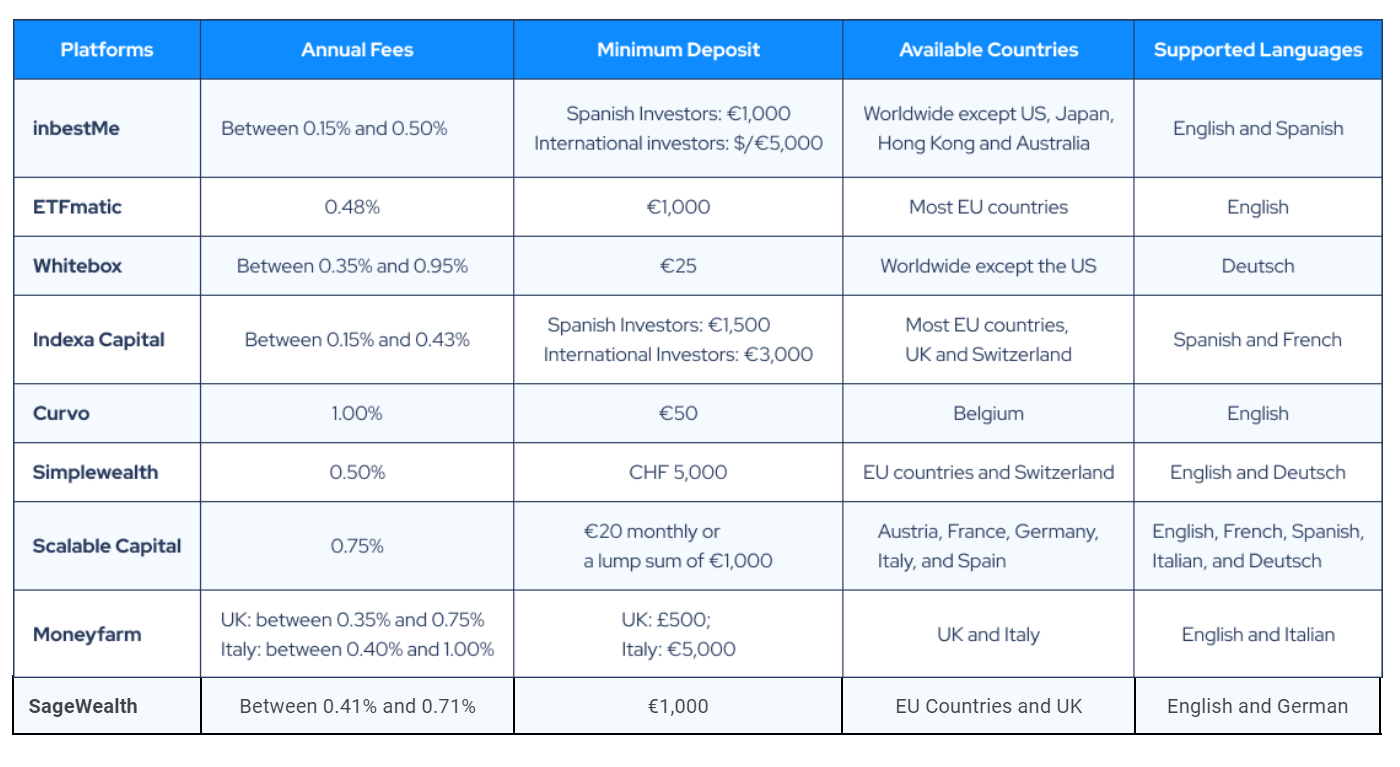

SageWealth fees compared to other European robo-advisors

As you can see in the table (original table without SageWealth), we are similarly priced to other European robo-advisors. Moreover, none of our competitors above offers free 1-on-1 consulting.

A key point to highlight is that we are using more sustainable ETFs. Most robo-advisors will use ETFs with a cost of 0.15%-0.20% per year. However, the ETFs at SageWealth are in the 0.23%-0.28% range. We think this increased cost is worth it for the reasons discussed above.

3.5 Regulatory perspective/details

Investment finance is complex and we are incorporated and based in Germany, (probably) the strictest regulated financial market in the world. To meet these requirements, we have partnered with two industry experts to ensure full legal compliance, safety, and flexibility.

- Our compliance partner is Bank für Vermögen, which monitors that all our legal processes are in compliance with regulations.

- All investments are held securely with our custodian bank, Baader Bank.

All parties are regulated by BaFin (Germany's financial supervisory authority). You can find our entry in BaFin’s directory of financial intermediaries.

Strictly speaking, we are a tied agent of Bank für Vermögen (BfV) and pay BfV a profit-sharing fee per client to process and monitor their accounts. However, we are independent in what and how we offer financial advice. We don’t receive a commission from BfV.

Our co-founder Sana Al-Badri is a certified financial advisor (according to German regulation §34f GewO) who can and does offer financial advice independently. That being said, in the name of transparency, given that we are offering investment portfolios, we have the incentive to advise potential clients to invest in these portfolios. However, we try to do this with as much integrity as possible and often advise people NOT to invest for the moment, or we recommend they invest elsewhere.

When you sign up with SageWealth, you open an account with Baader Bank. They are our custodian bank. All trades, deposits, and withdrawals are facilitated through their systems. Baader Bank is one of Germany's leading capital market banks and one of the largest market makers on Europe's key stock exchanges. We partnered with them because of their strong track record of working with Europe's biggest Fintechs.

This also means that your investments are not tied to the success or failure of SageWealth as a company, as they are held in a separate investment account at Baader Bank, under your own name. Moreover, EU regulation mandates that even in the unlikely event of bankruptcy of Baader Bank, your assets do not belong to them, and you will be given the opportunity to move your assets to another brokerage or liquidate the assets and withdraw your assets as cash.

3.6 Isn’t it cheaper to invest by myself on an online broker?

Yes! The annual fees of ETFs are between 0.15% to 0.30% per year. There is no avoiding these. However, you can invest either by yourself with an online broker, or you can use a robo-advisor / investing platform. With a broker you will pay €3 - €10 per trade; and with a SageWealth you would pay 0.41% - 0.71% per year in management fees.

Over the long-run it will be cheaper if you invest yourself with a broker, and there are good guides out there (and even some specifically for EAs).

In short: You need to open an online broker, such as Interactive Brokers, Degiro or Trade Republic. Then you have to choose your strategy and investment horizon (and stick with it!). Based on this you should research the ETFs available here (for both performance and sustainability), and pick them (you can use our portfolios above if you like). Finally, you have to buy and sell them as needed (it’s important that you also rebalance the portfolio once per year).

While we fully encourage people to invest by themselves, in our experience of speaking with hundreds of first-time investors, they mostly feel uncomfortable investing by themselves without guidance. And we think this is perfectly reasonable, as there is evidence showing that the average US investor who invested alone had a return of 2.9% pa, in the past 10 years. Which is significantly lower than the average market returns of 10.94% pa!

This is most likely due to emotional trading. We see first-hand that our users get cold feet when markets are volatile and have a tendency to buy when markets are high and sell when they are low. Working with an advisor can prevent that.

4. A personal note from the founders

We, Marco and Sana, are long-time effective altruists who have a knack for building stuff in a fast-paced environment. We loved our previous experience in start-ups and love building SageWealth.

Our EA mission is to build a start-up that has a net positive impact and then donate and invest the majority of the proceeds upon exit to highly impactful charities and startups. We call this a ‘Start-up to Give’. We are inspired by the likes of Niklas Adalberth (founder of Klarna), who took the Founders Pledge and went on to found an impact VC, which includes a branch that exclusively invests in African entrepreneurs (which is a hugely neglected investment space).

The biggest funders in EA are entrepreneurs (like Dustin Moskowitz) and we see interesting developments, such as EA angels who aim to invest in early-stage startups because of their huge financial upside (we pitched to them and received some funding). One should also not neglect the huge network successful entrepreneurs have - HNWIs, tech talent, top bankers, venture capitalists, and media - that can be leveraged for impactful outreach.

In 2013, Jess Whitlestone wrote for 80000 Hours that for-profit entrepreneurship is potentially one of the highest-earning careers, ‘more promising than other high-earning careers for doing good directly’, and ‘one of the best ways to build career capital early on in your career’.

However, running a startup is very risky, expensive, and has a high risk of burnout. For these reasons, we should be extra encouraging and supportive of EAs running start-ups, even if those start-ups themselves only have a marginal impact.

ESG today is not perfect, but we would be excited to work together with a large asset manager/insurer/pension fund on a new pension product for the young & digitally savvy market. This would be a chance to create an ESG product with better methods to calculate impact and could lead to investment products that include neglected risk factors such as AI risks, animal welfare, or global catastrophic biological risks, which are largely ignored in ESG today. The success and launch of such a product can be a case study for the rest of the industry and help promote EA values. Alternatively, it could be impactful to fund research to build an ESG framework from the ground-up based on EA frameworks.

We can see many more such paths, but the strong network we’re building ensures that we’re best positioned to tackle ESG challenges and support spreading EA values into the financial system. This matters because our values differ substantially from most FinTech founders in wealth management.

Over the last 3 years, we have already connected to high-ranking executives in all relevant institutions within ESG, such as asset managers and ESG rating agencies. They’re following our journey closely and some have even jumped in as investors.

We see that most investment platforms and financial institutions are unconcerned with maximising savings and donations. They don’t care about enabling impact-minded individuals to have more time and money to dedicate to their causes. In contrast, we are very much concerned about this and are currently in the process of offering profit-sharing donations and advising individuals on how to engage most effectively in investing to give.

As we grow and acquire more funding, we want to build tools specifically for people who need to take care of their own future while also honouring a pledge to donate (like many members of the EA or animal rights community).

Commonly asked questions

What if you go bankrupt?

In case SageWealth goes bankrupt, your investments will not be affected. You will retain your Baader Bank account, for which you receive log-in information to their portal. Upon bankruptcy, you can choose to keep your account at Baader Bank or transfer your assets to another brokerage of your choice. In case of a Baader Bank bankruptcy, you will still retain your assets, because they’re legally and infrastructurally separated from Baader Banks‘ assets. This means you can transfer your assets to another brokerage.

This may take several weeks and require some paperwork. Your investment is legally considered a ‘special asset’ (Sondervermögen) that is managed and accounted for separately from the assets of the investment company. This is part of a wider Europe-wide regulatory framework MiFID II/MIFIR.

What is your approach to sustainability? Why don’t you include nuclear energy or GMOs?

In short, we entirely exclude fossil fuels (sometimes gas can be included), weapons, tobacco, alcohol, gambling and animal agriculture. We write more about that on our website.

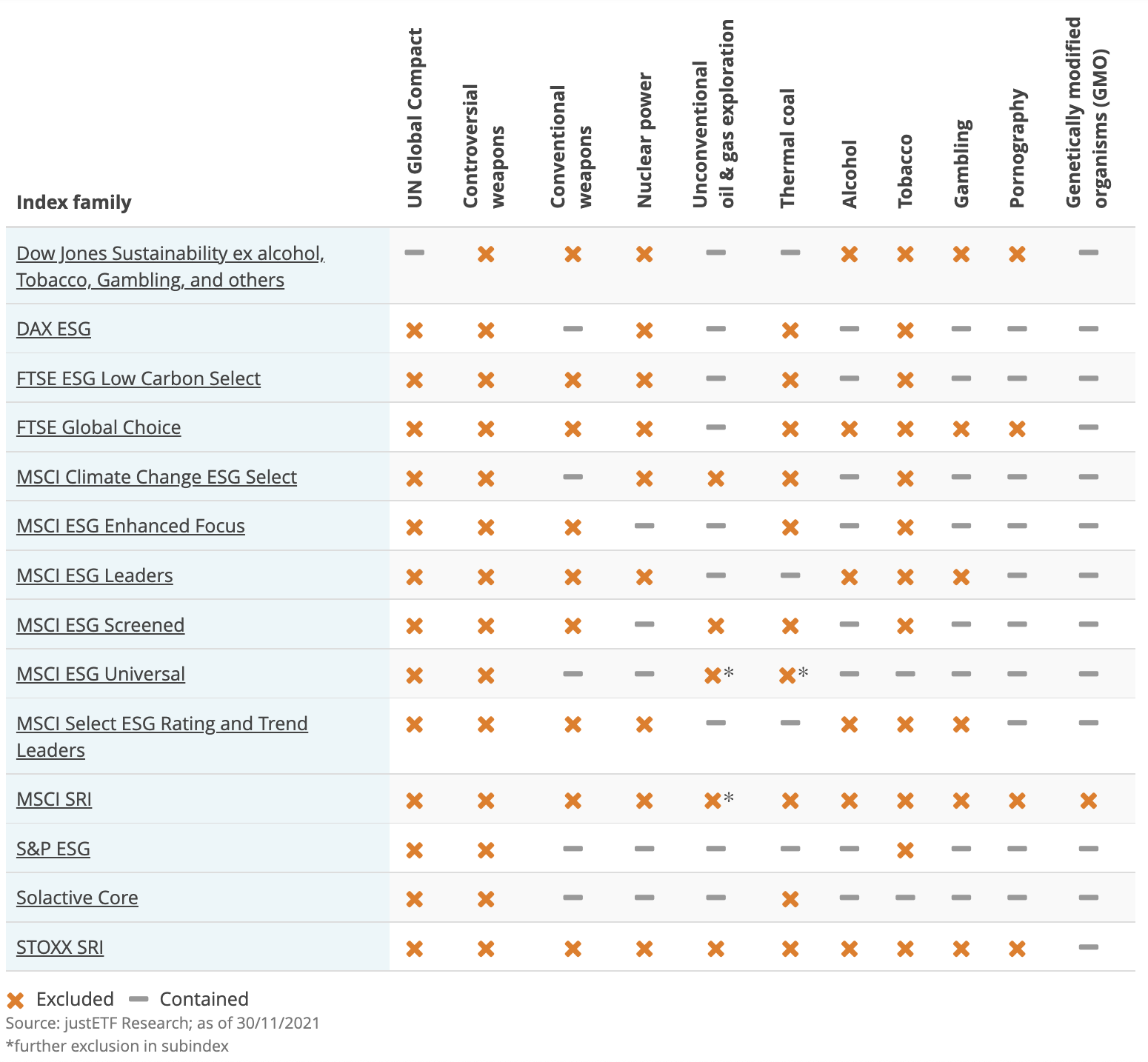

Among the excluded categories are also ones that we believe should not be excluded, such as nuclear energy and GMOs. While we personally are supportive of GMOs and nuclear power, it is difficult to find good sustainable ETFs that don't exclude those. Unfortunately, at our current company size, we have to deal with the constraints of the current state of the market. This is because as a small startup we need to choose from existing ETFs and cannot pick individual companies. As one can see in the table below, many sustainable indices exclude nuclear energy, and MSCI SRI, one of the most widely used indexes for sustainability, excludes GMOs.

Unlike other sustainable robo-advisors, we are monitoring the market, and are excited to include more scientifically-informed ETFs (that include GMOs or nuclear energy) as they become available on the market at a reasonable cost.

Did you take the Founders Pledge?

We would love to take the Founders Pledge! Unfortunately, given our small size as an early-stage startup, we are not yet eligible to do it formally.

What features are you working on to support Effective Altruists?

We are currently in advanced conversation with a prominent EA organisation to allow our users to donate a portion of their annual profits to high-impact charities at the end of the year. And we are working out a way to match donations as well. As far as we are aware, we are the only investment platform committed to adding such features. We want to learn more about what EAs need to better manage their personal finances and donations.

Is it realistic to expect that the markets will keep growing as they have in the past?

Nobody knows the future for certain and the average performance of the past is simply the best reasonable guess we can make. It is true that future technologies like AI and drones or biowarfare might seem threatening today. However, take for instance the S&P 500 Index performance of 406,766% (adjusted for inflation, dividends reinvested) from the year 1900 until 2022 which includes two world wars as well as the cold war era.

The truth is that humanity has faced many challenges before and so far has always found a way to fix things. And AI, biotech, or space flight might usher in an unprecedented era of abundance for humanity. We believe that investing in a widely diversified stock portfolio is one of the best things you can do with your money to benefit from that future.

In case the future is utterly dystopian, money would be most likely worthless, whether invested or not.

Doesn't the Efficient Market Hypothesis imply that we can't expect sustainable shares to do better in expectation because this information is already priced in?

As with the previous question, this might be true but there’s no way of knowing. We argue for sustainable stocks because the existing evidence shows they produced higher returns while having less risk. Also, they might have a marginally positive effect on the world.

Our personal opinion is that we’re underestimating the economic impact of climate change. As of now, there’s a funding gap of $270 trillion to meet net-zero targets by 2050. People have a tendency to discount the future, and this bias could be seen in the stock market right now.

Shouldn’t we really be influencing shareholders in these ‘bad’ companies instead of divesting them?

We think shareholder activism is a very promising cause area. However, consider that voting rights scale linearly with your invested capital. In other words, one billionaire can have as much impact as 100,000 people each investing 10.000 EUR of their savings.

With SageWealth we decided to focus on what impact you can have passively with your savings that would otherwise sit in your bank account while also remaining liquid.

Acknowledgements

This article was written by Marco Vega and Sana Al-Badri. Thanks to SageWealth employees Jan Beck and Julian Rosenberger von Papstein. Thanks to the valuable feedback we received from Devon Fritz, Lukas Trötzmüller, Leah Edgerton, and Patrick Gruban (who encouraged us to write this article).

We have previously attended the career fair of EAG London and San Francisco and held a talk titled 'Personal Finance & Sustainable Investing for EAs' at EAG X Berlin 2022. Some people we spoke to have expressed a wish that there should be guidelines for how for-profit companies interact with the EA community. We hope that with this article we add transparency to who and what we are and set a positive example. Above all else, we want to encourage an open discourse.

Change log

- 2022-12-20: Initial version published

Notes

- ^

Calculations are shown in section 1.3.

- ^

Income data from StepStone Income report 2022.

- ^

Assumptions: 9% p.a average market growth (80% of MSCI World’s historic 10.94% p.a.); Adjusted for 2% p.a. inflation; includes capital gains tax of 25% p.a. (German rate).

- ^

Assumptions: 9% p.a average market growth (80% of MSCI World’s historic 10.94% p.a.); Adjusted for 2% p.a. inflation; includes capital gains tax of 25% p.a. (German rate).

- ^

In ‘ESG-speak’, these are ESG risks most material to the company.

- ^

Note that SageWealth Growth did not exist prior to 2020. However, the ETFs and companies inside them did. As such, this is a backtest of the portfolio to see how it would have performed in the past.

- ^

Unfortunately, this means that 8/15 ETFs in the portfolio are issued by asset managers with ambiguous or poor voting records towards climate resolution and other responsible investment themes. We’re committed to improving this in our next iteration for stronger sustainability.

- ^

Sustainable ETFs are more expensive and we sacrifice profits to be able to offer them at lower costs to clients.

[Writing this in my personal capacity]

Thank you for publishing this! As you mentioned, I encouraged you to write this post. Still, I wouldn't recommend your company to people in the EA community, and I think giving SageWealth a stage at three EAG(x) conferences was wrong.

For the background: After meeting a team member and seeing that you were presenting at EAGx Berlin and had attended EAG career fairs, I tried to find out more about SageWealth. What I found made me concerned about values, transparency, and your targeting of members of the EA community as potential customers and employers. We spoke at EAGx Berlin (this was before I was offered the position as Co-Director EA Germany) and initially wrote a draft forum post about my concerns that I shelved when you shared the draft of this post.

I think it's great that you're building up a business and plan to donate. Being an entrepreneur myself, I very much appreciate this. Encouraging people to invest in globally diversified investment products is something I also do, and having an easy-to-use product can make the difference between someone thinking about investing and not doing it.

However, promoting your commercial product or job opportunities within the EA community mixes your intent of donating and the product you sell. The product is similar to others in the market that are less expensive. If someone asks me for advice, I would point them to competitors or would recommend investing in ETFs directly.

I'm much more excited about people that don't sell products but educate people to invest. For example, Rebecca Herbst teaches financial literacy and donates all proceeds to The Life You Can Save with her service Yield & Spread.

I won't go into details concerning your product. But I do want to point (as I did in the draft you shared with me) out that I find it concerning that your view on nuclear energy and GMOs differ from this post where you say they shouldn't be excluded and your website, where you describe them as part of "the worst offenders". Perhaps you have to conceal the truth to sell your product, but then your target market shouldn't be truth-seeking people in the EA community.

Hi Patrick,

Thank you sharing your thoughts here. We appreciate your feedback on SageWealth and how we can relate to the EA community. Some thoughts on your points:

Regarding your sentiment that "it was wrong" for us to attend EAG(x). We would like to clarify that we did not initially build SageWealth with EAs in mind. However, gradually over time, we noticed a lot of interest coming from EAs in our circle - many who were booking advisory calls and opening accounts. This eventually led to the realization that EAs could really benefit from a platform like ours, and we decided to participate in EA events. We are 100% supportive of educational platforms like "Yield & Spread", but also noticed that most people it's not enough to just learn about investing, and they need more guidance and a platform that helps put things into action. We understand the 'skepticism' that kicks-in because we are a for-profit. But the truth is that we are better able to solve people's core problem by building a technical platform that makes the investment process easier!

Taking a step back, I think the main issue here is that there are no guidelines on how a for-profit can engage with the EA community. We simply applied and got accepted. We would be excited to be part of this conversation. I'm sensing an implicit assumption that simply by being a 'for-profit' that we are a corrupting force, when in reality the world is filled with businesses that are serving peoples' needs and solving problems. We believe that we can be a positive force in the community, by helping EAs better retire and grow their wealth for donations, and don't think our for-profit positioning runs counter to these benefits.

And lastly, we appreciate your point on nuclear energy and GMOs. This feedback is helpful, and we have now amended our sustainability article for consistency.

While I appreciate the investment thoughts in this post, I strongly downvoted it because I don't think the EA forum is an appropriate place to advertise specific financial products.

Or at least, I don't understand why I should use this one over others.

Thanks for your comment. We plan on adding EA-specific donation features that would sell-off a certain percentage of your portfolio to automatically donate to a highly effective charity. Also, we are working on a retirement calculator that would take your donation goals into account. Would either of these be useful to you?

Not useful enough to make me use it.

Thanks for your comment. If I may ask, would you have upvoted if we had split sections 1&2 into their own posts and only linked to sections 3&4 externally? Regarding your point on advertisement: If, for example, I wrote a post on how to run local groups more effectively using the productivity software that I also happened to sell, would this also cross the line? Is it ever OK for an EA to want to share their solution with the community if it is a for-profit?

If sections 1 and 2 were their own post, I wouldn't have strongly downvoted, but I probably wouldn't have upvoted either. Investing advice isn't new or interesting to me.

There is some interest in investing; our local group even ran a 6-week course on socially responsible investing in the fall that was well received. Importantly, the person giving it didn't use it as an advertising opportunity. They were just genuinely interested it the topic and sharing what they learned.

Is it ever ok for EAs to share one of their for-profit solutions? Yes, but generally only in response to a specific request. For example, if someone posts on the EA groups slack channel they are interested in productivity resources, it would be ok to mention your productivity tool in response. Unprovoked advertising is never well received, because advertising doesn't have the best interest of the audience in mind.

TLDR: I appreciate Marco, Sana & SageWealth, but do think that this is probably not a good place to advertise such products (based a.o. on feedback from their talk at EAGxBerlin)

Marco's co-founder Sana gave a talk at EAGxBerlin 2022, and as event lead, I read through all participant feedback. This was one of the more controversial sessions at EAGxBerlin- some (especially those new to investing) found it quite helpful, while others (including some with more investing expertise) were more critical for various reasons.

I don't know enough about SageWealth's products to have an informed opinion. Just from reading through the EAGx feedback and comments here, I do share the general sentiment that EA spaces like EAGx or this forum are probably not good places to advertise such products (unless you want to be totally truth-seeking and also include all the reasons against buying the product, alternative products from other companies etc).

I do agree that many EAs probably underestimate the benefits of investing their savings (rather than just keeping them sitting idle on a bank account), and I appreciate Marco & Sagewealth for bringing attention to this! I'm also glad to have Marco & Sana in the EA community - I've met them often on various events around Berlin, had many interesting conversations and always enjoyed their company :)

PS: I wonder if you could do both raising awareness of "investing to give" and advertising your products in different posts, without one affecting the other? I think this might be worth a try. You could include disclaimers wherever relevant.